Billionaire Bill Ackman of Pershing Square Capital has been calling for the turnaround of the mega-cap consumer products company The Procter & Gamble Company (NYSE:PG) for some time now. At the Sohn Investment Conference last week he reiterated his position on P&G, calling out the CEO Bob McDonald.

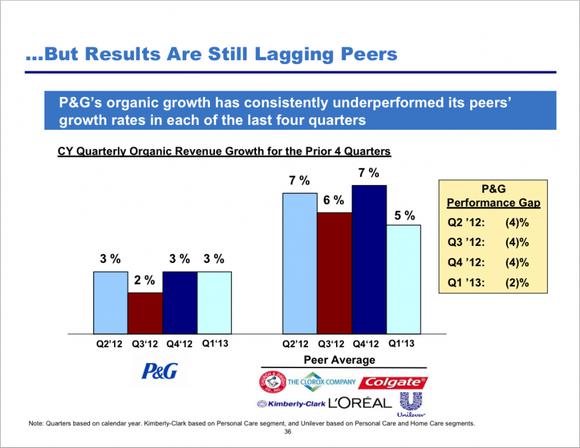

Ackman’s comments at the Sohn conference said he was willing to give CEO McDonald two to three quarters to get the company in “better shape.” Of course, that’s a relative term, but by better shape, Ackman wants to see at least 5% annualized revenue growth and major cost cutting. Part of Ackman’s displeasure includes the fact that The Procter & Gamble Company (NYSE:PG) has underperformed its major peers over the past four quarters.

One of Ackman’s big gripes about McDonald is that he has served on 21 different organization boards, which includes Xerox Corporation (NYSE:XRX) as of early 2012. Ackman thinks this number is excessive. At Sohn, Ackman noted that “we make the conservative assumption that just attending board meetings and not including travel time, this accounts for 25% of his time.”

Ackman believes that If McDonald and the board can strategically refocus the company and cut costs effectively, the company has tremendous upside.

The positives

One of the positives of The Procter & Gamble Company (NYSE:PG), as Ackman has noted, is the company’s exposure to emerging markets.

P&G hopes to further increase its presence in these fast-growing markets, helping diversify away from the weakening North America and Western Europe markets. P&G’s developing-market sales have grown at a compounded average growth rate of 12% over the last 12 years and its current exposure is one of the industry’s best.

The after-tax profits in its top-10 developing markets are also expected to increase by 35% in fiscal 2013 versus 2012 behind increased marketing investments and innovation.

The comps

Two of The Procter & Gamble Company (NYSE:PG)’s top competitors include Johnson & Johnson (NYSE:JNJ) and Colgate-Palmolive Company (NYSE:CL). Johnson & Johnson has unique exposure to a variety of industries, not just consumer products, but also the pharmaceutical and medical-device industry. Its medical-device segment accounts for more than 40% of revenues. This segment offers wound care and minimally invasive surgical products, as well as orthopedics and diagnostics.

One possible setback for Johnson & Johnson (NYSE:JNJ) is its exposure to the pharma industry, which accounts for over 37% of revenues. The company has seen a number of setbacks in its drug pipeline, which includes failure to gain approval for ceftobiprole, a second complete response letter (CRL) for the supplemental new drug application (sNDA) for Xarelto for acute coronary syndrome (ACS), and the withdrawal of the EU application for an additional indication for Velcade for the treatment of patients with relapsed follicular non-Hodgkin lymphoma.

Even after posting better-than-expected 2012 earnings and first-quarter 2013 earnings that beat expectations, Johnson & Johnson (NYSE:JNJ) maintained, versus upping, its 2013 earnings guidance at $5.35 to $5.45 per share.

Colgate-Palmolive Company (NYSE:CL) gets the majority of its revenues, over 25%, from Latin America, which is a long-term positive as the country continues to develop. As well, the consumer-products company has one of the leading positions in oral and personal care.

Colgate managed to post first-quarter 2013 earnings of $1.32 per share, which was up 6% year over year. The company also saw its gross profit margin expand by 40 basis points to 58.6%. The big positive for the company is that it expects to continue posting impressive growth. For 2013, management expects the company to see 5.5% to 6.5% growth in earnings year over year.

However, The Procter & Gamble Company (NYSE:PG) is the best-priced stock of the three, trading cheaper than its peers on both a price-to-earnings and price-to-operating-cash-flow basis.

| P&G | Johnson & Johnson | Colgate-Palmolvie | |

| Price to earnings | 19.8 | 23.2 | 24.6 |

| Price to operating cash flow | 14.7 | 16.4 | 20.4 |

Although Ackman has been the “loudest” P&G shareholder of late, he’s not the largest hedge fund owner of P&G by shares. Fellow billionaire Warren Buffett owns almost double the shares of Ackman (check out Buffett’s high upside picks). Meanwhile, Johnson & Johnson (NYSE:JNJ) has billionaire Ken Fisher (see Fisher’s cheap stock picks) as its top fund owner, and Colgate-Palmolive Company (NYSE:CL) calls Lansdowne Partners its top hedge fund shareholder by shares.

Ackman’s thesis

Ackman believes the company is under-earning relative to its intrinsic earnings power. He believes that with strategic initiatives the company could easily grow earnings from from $4 per share to $6 over the next couple of years.

If the company is able to reach this earnings potential of $6 per share, Ackman also sees the company being able to achieve an intrinsic value of $125 per share in approximately two years, suggesting around 60% upside.

Don’t be fooled

Although the upside sounds very appealing, The Procter & Gamble Company (NYSE:PG) still has a lot of work to do if it plans to meet Ackman’s expectations. After posting first-quarter earnings, P&G tightened its core 2013 earnings guidance from $3.94 – $4.04 per share to $3.96 – $4.04. However, to help turn the company around, P&G is now focusing on its 40 largest and profitable businesses.

These businesses account for about 50% of sales and 70% of operating profit. The company is also concentrating on its 10 most important developing markets, which should help drive Ackman’s expected robust revenue growth. Although I think it will be tough for P&G to hit Ackman’s targets over the next couple of years, even if the stock doesn’t hit the $125 Ackman target, if it at least reaches $100, that’s still 25% upside.

The article Billionaire Bill Ackman: CEO’s Clock Is Ticking originally appeared on Fool.com and is written by Marshall Hargrave.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.