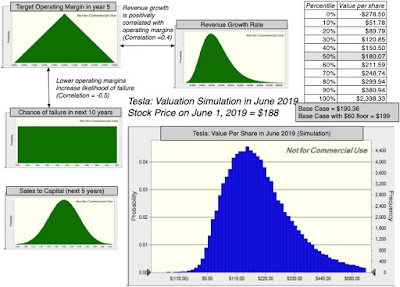

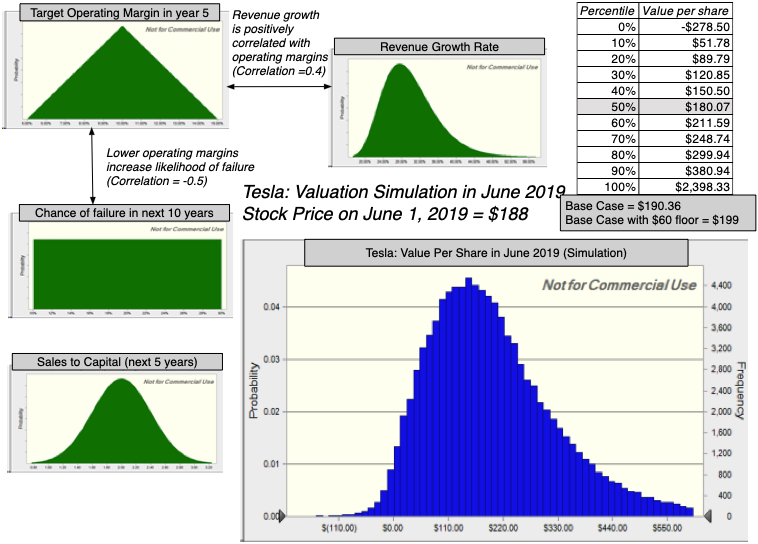

As you can see, I borrow from both sides of this debate, and I am sure that Tesla bulls will be disappointed that I don’t have higher revenues for the company and Tesla bears will take issue with my reinvestment assumptions and expectations that the company will eventually deliver solid margins. Using a technique that I find useful, when confronted with divergent views, to deal with uncertainties, I computed Tesla’s values in a simulation, with the results below:

in summary, the median value across the 100,000 simulations is $180/share, the 10th percentile delivering a $52 value/share and the 90th yielding $380/share. In this simulation, I have assumed that Tesla will remain a stand alone, going concern, and that the equity value could drop to zero, if there is a shock to the value of operating assets, given the debt load. There is talk, however, that Tesla could become an acquisition target, to an automobile company or a tech company (see this rumor about Apple being interested in 2014).

While there are some entanglements (such as the one with Panasonic in the battery factories) that will have to be worked out, there have generally been two impediments on this path. One is that Tesla has been an expensive target, especially when its market capitalization exceeded $50 billion. That will become less of a barrier, as the stock price drops, and at a market cap of less than $15 billion, it could be much more affordable. The other is a bigger and more intractable problem. With Elon Musk as part of the package, Tesla has a poison pill that few companies will want to imbibe, and it is likely that the relationship will have to be severed or at least significantly weakened for an acquisition to occur. I remain skeptical on the odds of an acquisition, precisely because I don’t see Musk going quietly into the night, but adding an acquisition floor at a $15 billion value for equity (about $60/share) increases the simulated value for the stock by about $10/share.

3. The ARK Tesla Pricing

It is not my role to be an arbiter of other people’s valuations, and I generally avoid commenting on them unless they are in the public domain, as was the case with the Tesla/Solar City fairness opinions, or seek public comment. I will make an exception with the ARK “valuation” of Tesla, partly because they are among the stock’s strongest boosters and partly because they put their model up for public comments, for which I commend them. In summary, here are the ARK numbers:

|

| Download ARK pricing from Github |

- This is a pricing, not a valuation: I know that this will strike some as nitpicking but what ARK has produced is a forward pricing for Tesla, not a valuation. An intrinsic valuation requires forecasting cash flows over time, after taxes and reinvestment, and then discounting those cash flows back at a rate that reflects the risk in the investment. A pricing usually involves picking a metric (revenues, earnings, EBITDA), picking a forecast year for the metric and applying a multiple based upon what other companies in the peer group trade at. ARK’s basic model forecasts revenues, earnings and other metrics in 2023, and applies a multiple to estimated EBITDAR&D in 2023, making it a forward pricing.

- The ARK bear is bullish: The ARK bear case requires that Tesla will sell 1.7 million cars in 2023, at an average price of $50,000/car and generate an operating margin of 6.1% on those revenues. Each of these assumptions is plausible, and the combination is possible, though to call a seven fold increase in revenues over five years, with a concurrent improvement to industry average profitability, a bear case seems to be stretching the definition of bear.

- The weakest link: The model’s weakest link is on cash flows, since to sell 1.7 million cars, you have to make them first, and Tesla’s production capacity, even if you count the China plant as functional and about the same capacity as the Fremont plant, brings you only about half way to the goal. It will be magical, if adding another $3.7 billion to net PP&E (as ARK seems to be assuming) and $1.2 billion to working capital will allow you to increase revenues by $63.5 billion, but it gets even more stretched, when you assume that Tesla also pays off $14 billion in debt (as ARK seems to) over the five years. In sum, the bear case will require at the very least $25 to $30 billion in cash flows, even with ARK’s own assumptions, over the next five years, and since the operating cash flows at the company are still a trickle, this will require equity issuances in massive proportions fairly soon. ARK does allow for an equity capital raise of $10.6 billion which strikes me as too little to fill the gap, but in the absence of a balance sheet or statements of cash flows, I may be missing something (and it has to be very big).

- Share count issue: Even for the equity capital raise of $10.6 billion, ARK reduces the impact on share count by assuming a stock price of $360/share (market cap will be $70 billion) at the time of the raise. Since this capital will have to be raised soon, there is an element of wishful thinking here, i.e., that stock prices will double in short order and the capital raise will follow. In addition, if stock prices do climb, as ARK assumes, there will there is an overhang of 20 million options that have been granted to Musk by the board of directors that will become actual shares. In short, for the ARK bear case to unfold, the share count will have to double over the next five years.

- There is a time value question: Applying a multiple to EBITDAR&D in 2023 gives you a value in 2023, and to make it comparable to today’s stock price, you will have to discount it back to today, at a risk adjusted rate. In fact, if you bring in the probability of failure embedded in Tesla bonds, there will an additional discounting on value.