Note the divergence in both the overall ratings and on the individual metrics (E, S and G) across the services, even for widely tracked companies like Facebook and Walmart. There are some who believe that this reflects a measurement process that is still evolving, and that as companies provide more disclosure on ESG data and ESG measurement services mature, there will be consensus. I don’t believe it! After all, what I find to be good or bad in a company will reflect my personal values and morality scales, and the choices I make will be different from your choices, and any notion that there will be consensus on these measures is a pipe dream.

Even if you overlook disagreements on ESG as growing pains, there is one more component that adds noise to the mix and that is the direction of causality: Do companies perform better because they are socially conscious (good) companies, or do companies that are doing well find it easier to do good? Put simply, if ESG metrics are based upon actions/measures that companies that are doing better, either operationally and/or in markets, can perform/deliver more easily than companies that are doing badly, researchers will find that ESG and performance move together, but it is not ESG that is causing good performance, but good performance which is allowing companies to be socially good.

The ESG Sales Pitch – Promises and Contradictions

The power of the ESG sales pitch has always been that it offers something good to everyone involved, from companies adopting its practices, to investors in those companies, and more broadly, to all of society.

– For companies, the promise is that being “good” will generate higher profits for the company, at least in the long term, with lower risk, and thus make them more valuable businesses.

– For investors in these companies, the promise is that investing in “good” companies will generate higher returns than investing in “bad” or middling companies.

– For society, the promise is that not only will good companies help fight problems directly related to ESG, like climate change and low wages, but also counter more general problems like income inequality and uneven healthcare.

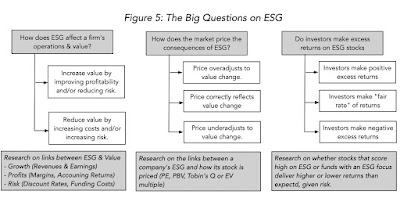

Given that ESG has been marketed as all things good, to all people, it is no surprise that its usage has soared, with companies signing on in droves to social compacts, and investors pouring hundreds of billions of dollars into ESG funds and investments. In the process, though, its advocates have either glossed over, or mixed up, three separate questions that need to be answered, on ESG:

The reason it is useful to separate the three questions is that it opens up possibilities that are often missed in both debate and research. For instance, it is possible that ESG does nothing for value, but that it offers a sheen to companies that allows them to be priced more highly than their less socially conscious counterparts and enriches investors, who trade on its basis. Alternatively, it is also possible that ESG does increase value, but that markets adjust quickly to this and that investors do not benefit from investing in ESG stocks. It also illustrates the danger of overreach from ESG research. Much of the research on ESG is compartmentalized, where only one of these questions is addressed, but the researchers seem to use the results to draw conclusions about answers the other two. Thus, a research study that finds that investors make higher returns on companies that rank high on ESG often will go on to posit that this must mean that ESG increases value, a leap that is neither justified nor warranted.

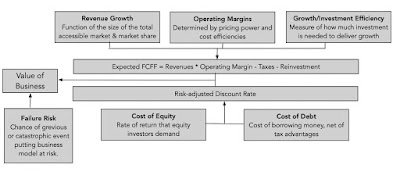

ESG and Value

The framework for answering the question of whether ESG affects value is no different from the framework for assessing whether acquisitions or financing or any other action affects value. It is both simple and universal, and I have captured the drivers of value for any business in the picture below:

|

| Figure 1: The Drivers of Value |