In 2005, Southwestern Bell (SBC) Communications acquired AT&T Inc. (NYSE:T) in a $16 billion transaction to “create the industry’s premier communications and networking company,” as described by AT&T. Shortly afterwards, SBC changed its name to AT&T. At that time, the AT&T management team was hungry for bulk through acquisition, investors were unhappy with the price paid for acquiring Cingular, and the Motley Fool recommended AT&T as a sell “until the company gets its arms around the new businesses.” It has been seven years since that recommendation. Has AT&T got its arms around the new businesses yet? Let’s see.

The AT&T Inc. (NYSE:T) of today is a multinational telecommunications corporation ranked in 2012 as the biggest telecommunications company in the United States, in relation to its revenue ($126 billion in 2012), and the 32nd largest company in the world, according to CNN. It is a leading IP-based communications service for businesses, has a large 4G network, and has over 30,000 AT&T Wi-Fi Hot Spots. As a result, AT&T is a common household name. In addition, AT&T is a component of the Dow Jones industrial average.

U-Verse

If that isn’t enough, AT&T has developed and is currently marketing its U-Verse TV. U-Verse TV is AT&T’s digital TV service that receives information via fiber optic technology. U-verse includes IPTV services, IP telephone and broadband Internet. Consequently, U-verse TV can support up to four active streams at the same time–an important aspect for many subscribers.

AT&T has been focusing a lot of its effort and money as of late on advertising U-Verse. This spending is paying off, as it has reported strong growth in U-Verse. More specifically, in 2011, U-Verse was available to over 30 million people in 22 states; at that time, it had 3.8 million subscribers. During the first quarter of 2013, AT&T Inc. (NYSE:T) had 8.7 million U-Verse subscribers. Hence, it more than doubled its subscriber numbers in less than two years. It strives to continue this trend.

While its U-Verse subscriptions are growing, these numbers are still distant from the 107 million wireless subscribers AT&T had in the first quarter of 2013. That being said, U-Verse and wireless are currently driving AT&T’s revenue.

Dividends

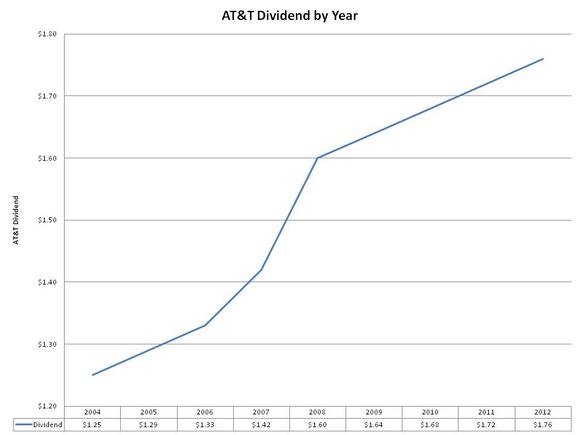

Alongside U-Verse, wireless and other AT&T telecommunication products, AT&T also has a great dividend. This dividend has increased every year since 2005, rising in that period from $1.29 to $1.76. Because of this dividend, DividendRank recently (June 11) put AT&T on its “S.A.F.E. 25” list, indicating that AT&T Inc. (NYSE:T) is a company with a strong 5% yield that has a (S) solid return, an (A) accelerating dividend amount over time, a (F) flawless history of not missing a dividend or lowering a dividend, and an (E) enduring quality, with a minimum of 20 years of dividend payments. In other words, the firm recommends AT&T as a safe investment with a strong dividend.

iPhone

In looking into AT&T’s dividend in more depth over the past decade, it can be seen that AT&T’s biggest dividend shift increase occurred after 2007. This was the same year it signed an exclusivity agreement with Apple Inc. (NASDAQ:AAPL) to be the carrier for its newly released iPhone. AT&T’s exclusivity agreement with Apple no longer exists, but Apple does currently have “non-exclusive” contracts with both AT&T and AT&T’s competitor, Verizon Communications Inc. (NYSE:VZ), the second-largest telecommunications company in the U.S. (revenue of $110 billion in 2012).

These non-exclusive contracts with Apple are significant assets to both AT&T and Verizon. Currently, Apple iPhone activations represent over 70% of AT&T Inc. (NYSE:T)’s smartphone customer base, which was approximately 3.7 million of its total 5.1 million smartphones sold in the first quarter of 2013. Verizon activated 7.2 million smartphone’s in the first quarter of 2013, with approximately 4 million being iPhones.

Competitor advances

In terms of competitor technology advances, Verizon is currently investing $100 million in “a solar and fuel-cell energy project that will help power 19 of its facilities in seven states,” according to Verizon. This is Verizon’s biggest commitment to clean power projects. It will allow Verizon to substantially offset its carbon emissions footprint by the equivalent of 3,000 passenger cars annually. Verizon is forward thinking with this project, as it expects a return on this investment in 10 years in terms of no longer paying other electricity companies for their power. It will also help with off grid resiliency; which has been deemed an important aspect over the last two decades.

Verizon is also putting together a new bid to buy out Vodafone Group Plc (ADR) (NASDAQ:VOD)’s Verizon Wireless shares after its proposed $100 billion bid was rejected in April. Consequently, Vodafone’s shares have been increasing since talks of this buy out earlier in the year. This buyout is expected to bolster Verizon’s growth.

Other competitor advances

Another competitor technology advance is the powering of the electric vehicle by Vodafone, India’s “first truly ‘connected car,’” with its machine-to-machine (M2M) communication services, which directly involves a strategic technology partnership with Mahindra Reva Electric Vehicles. This means drivers can use a smartphone app to remotely access features such as locking and unlocking doors, finding the closest charging station and checking the charge on a battery. This partnership is expected to significantly increase Vodafone’s revenue.

Conclusion

AT&T Inc. (NYSE:T) has been changing with the times, as we can see when it partnered with Apple and when it developed the U-Verse TV; there is no reason to believe that it will not continue to be at the forefront of telecommunications advances. It does have its competition, but competition is good, especially in the telecommunications arena, as it has led to many great technology advances.

I do believe that AT&T has changed a lot since 2005 and the original “sell” recommendation can be reconsidered. I believe AT&T is a good long-term investment that comes with the bonus of a good dividend, a dividend that helped put AT&T Inc. (NYSE:T) on DividendRank’s “S.A.F.E. 25” stock list.

Pamela Kaval has no position in any stocks mentioned. The Motley Fool recommends Vodafone.

The article Should We Reconsider AT&T? originally appeared on Fool.com.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.