Retail is one of the sectors that it pays to have an open mind over. In other words don’t let your built-in ideas and prejudices take precedence over the hard facts. Sometimes retail trends develop that we can’t personally foresee or understand. It is worth approaching NIKE, Inc. (NYSE:NKE) with these thoughts in mind. There are three key trends that investors need to appreciate about this company and will guide its performance going forward.

Three Things About Nike

I’ve been looking at Nike over the last year, and the three things that strike me about its performance are:

Chinese sales have weakened substantially, and since they tend to be relatively high margin this has had a disproportionate effect.

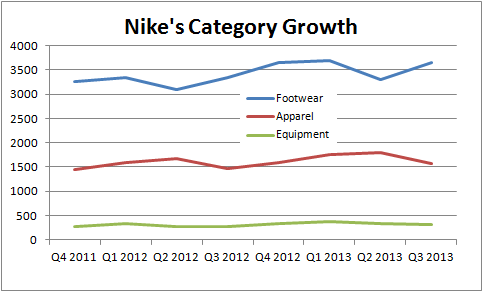

The strong performance in the last quarter was largely due to footwear sales. Footwear is a hot category in retail right now, and Nike has been doing particularly well with it. Apparel performance (particularly ex-US) hasn’t been as good. This has been somewhat surprising given the strength of other outwear brands.

NIKE, Inc. (NYSE:NKE)’s growth is somewhat contingent upon which sports it is strong in and, of those, which is trending well.

A Weak Chinese Consumer?

A graphical summary of Nike’s performance in China:

Note how sales start to drop off in the last calendar year and that China’s share EBIT is much larger than its revenue share. In other words China is very important for NIKE, Inc. (NYSE:NKE). It is also a long term strategic play for the company, and management spent a lot of time discussing the plans to reset the merchandise. The main focus of inventory management will be on China, and investors can expect to see some margin erosion in the region as inventory is sold off.

The wider question is whether this is a function of NIKE, Inc. (NYSE:NKE) getting its merchandising wrong or if it is a problem of a slowing Chinese consumer. Nike is not alone in seeing a downgrade of expectations. Other companies like McDonald’s Corporation (NYSE:MCD), Yum! Brands, Inc. (NYSE:YUM) and V.F.Corp have all reported weaker sales in China.

For Yum, this trend was in place even before the recent chicken supplier controversy in the country. Of course. this is somewhat problematic for Yum because China is the focal point of its sales efforts. It has no option but to try to ride through the controversy and carry on expanding even while same store sales growth is slowing. McDonald’s has also seen some negative numbers in China, and V.F. Corp reported an inventory build-up in jeans wear thanks to slowing sales growth.

It is not entirely clear whether this is a macro issue or a NIKE, Inc. (NYSE:NKE) merchandising one.

Best Foot Forward

If I had a dollar for every time I heard a retailer or department store talk about expansion plans with its footwear then I would start saving for my latest pair of Laszlo Vass shoes. As discussed in the intro this is not the sort of insight that I would intrinsically know, but when you hear companies like Coach, Inc. (NYSE:COH) talking about expanding its footwear range then you know that the consumer is spending on shoes in a way that she is not elsewhere.

It’s clear from this chart that the reason for the decent performance is due to footwear. Indeed, apart from China and Japan, every region reported good growth in footwear, from Central and Eastern Europe (up 8%) to North America (up 15%).

The bounce-back is largely due to successful footwear launches and the ongoing strength of running and basketball for Nike. I suspect the former’s success is due to the popularity of new product launches kicking in while NIKE, Inc. (NYSE:NKE)’s success in basketball shoes is partly a function of its significant investment in sponsoring players that achieved high profiles in the NBA season.

Where Nike Is Strong

Another key point to note is that outside of North America, apparel sales are not doing well at all. I’ve stripped out North America from the chart below to demonstrate this.

I was surprised by this because a company like V.F. Corp has been doing well internationally with the North Face and Vans shoes. The ongoing onslaught of the shift towards casual attire (you can tell I don’t like it) appears to be gathering pace.

My take on this is that consumers are becoming more specialized in their casual attire. For example, if you want to look like a skateboarder while driving your 4×4, buy Vans. Climbing Mount Everest before a trip to a coffee shop? Buy a North Face jacket. As a consequence Nike could be losing its appeal as an all purpose outwear brand.

Where Nike is not losing its appeal is in sports like basketball. The sports strength in North America goes some way in explaining why it is doing particularly well. In order to grow internationally it will have to connect emotionally with the sports that are popular in various markets and this requires marketing and sponsorship dollars.

Where Next for Nike?

The recent results were ahead of estimates, but NIKE, Inc. (NYSE:NKE) still has a lot of work to do in solving its problems in China, and there is a sense that the easy growth is over in the country. Moreover, strength in North America is great, but investors should not assume that this will translate internationally.

Having mentioned revenue growth in the high single-digits with earnings growing in the mid-teens for 2014, Nike will have to confirm this at the next set of results.

The article A Deeper Look at This Retailer’s Performance originally appeared on Fool.com and is written by Lee Samaha.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.