There is a lot to like about the long-term prospects for spice and seasoning company McCormick & Company, Incorporated (NYSE:MKC). Consumers are demanding ever more flavor in their cooking, and food companies are being forced to innovate by using flavorings in order to compete in difficult end markets. With these positive trends in place, the company is doing well. But what of its near-term prospects? Moreover, is the stock good value right now?

McCormick delivers mixed results

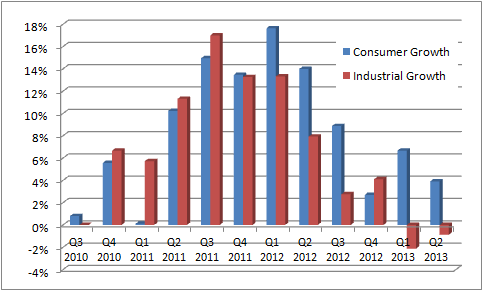

It was an underwhelming set of second-quarter (Q2) results for McCormick, as reported sales rose a paltry 2%. Its top line growth has been slowing in recent quarters as it laps some difficult comparables. In addition, Yum! Brands, Inc. (NYSE:YUM), is one of its major clients and it’s having some well documented difficulties in China with its KFC stores. First it was a scare over its chicken suppliers, and now it has to deal with fears over bird flu. The issue is hurting Yum!, and McCormick’s industrial sales are being hit because it supplies spices and seasonings to KFC.

I’ve broken out the progression of McCormick’s divisional sales growth below.

The problems in the industrial division aren’t just about quick-service restaurants in China, because McCormick’s industrial sales in the Americas declined 1%. McCormick & Company, Incorporated (NYSE:MKC) cited strength in its snack seasonings and food flavorings, but it wasn’t enough to offset declines in demand from quick service restaurants in the Americas. The eating out category has faced some weaker growth and, the areas that are growing within it are not favoring McCormick.

All of which is not to be too negative on the stock because it’s the consumer side that makes the majority of profits. And it is still doing quite well.

A breakout of Q2 operating income here.

Consumer segment sales grew 5% in constant currency. Within developed markets, McCormick is benefiting from a increased willingness among consumers to eat at home and, to utilize more flavors in their cooking. The latter trend is also being driven by an increasingly ethnically diverse population in many developed countries.

Within emerging markets, McCormick & Company, Incorporated (NYSE:MKC) is seeing good results via a mix of organic and acquisition-led growth. For example, in India its acquisition of spice company Kohinoor is giving McCormick long-term opportunities in an important growth market. India makes up less that 5% of sales, so there is plenty of scale for this figure to increase in future years. Similarly, the WAPC acquisition in China is believed to bring its Chinese sales up to 7% of the company total.

Two concerns

The first relates to the disappointing performance within China and the Americas on the industrial side. The hope with Yum! is that it will be able to recover from its company specific issues but I think there might be some macro factors at play here too. Yum! Brands’ same-store sales in China were getting weaker even before the media scare stories and bird flu worries hit.

It was a similar story with McDonald’s Corporation (NYSE:MCD).

The outlook for the quick service restaurant sector is important to McCormick, since much of its industrial demand goes to this industry. The signs are that it is not just a Yum! issue. McDonalds’s could be facing a tough year this year, and Yum! investors need to take note.

McDonald’s management was very clear on its last earnings call that it intends to retain and even grow market share. This as a sign that it will be willing to sacrifice margins and cash flow in order to secure long term positioning. McDonald’s and Yum! are likely to increase competitive efforts in North America in order to try and make up weakness elsewhere. McCormick & Company, Incorporated (NYSE:MKC) investors will be hoping that Yum! wins out.

The second concern is that even though the consumer division is doing well, its growth is still slowing. The company announced it was increasing incremental marketing on its consumer brands to $15 million but, it did not raise revenue expectations. The weakness on the industrial side is increasing the pressure on the consumer side.Is this marketing increase a sign that it is having to work harder to hit its numbers?

The bottom line

I don’t want to appear too negative here, because this company has plenty of good long-term drivers, and its acquisition strategy makes perfect sense. However, if you are going to add this stock to your portfolio, you will need to assess it on a risk/reward basis. This is a stock that trades at 22 times its November 2013 earnings, which looks pricey when compared to International Flavors & Fragrances Inc (NYSE:IFF)’s forward PE of nearly 18, and German rival Symrise at 20 estimated 2013 earnings.

McCormick & Company, Incorporated (NYSE:MKC) is hardly cheap, and its underlying growth is slowing while its end-market customers (on the industrial side) are facing some difficult market conditions. This stock is worth monitoring for a long-term buy, but an entry point might only come should it miss estimates this year.

The article Why This Stock’s Valuation Is Looking A Bit Too Spicy originally appeared on Fool.com and is written by Lee Samaha.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends McCormick and (NYSE:MKC) McDonald’s. The Motley Fool owns shares of McDonald’s. Lee is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.