Valued at $14.75 billion, L Brands Inc (NYSE:LTD)‘ robust and strong business model possesses a TTM profit margin of 7.20%. Recently, L Brands announced an increase in the company’s quarterly dividend payouts from $0.25 to $0.30, demonstrating the financial strength of the company.

So with the stock coming within dollars of all-time highs, is L Brands a tremendous play on the specialty retail industry, or should investors wait for a considerable pullback?

Strengths

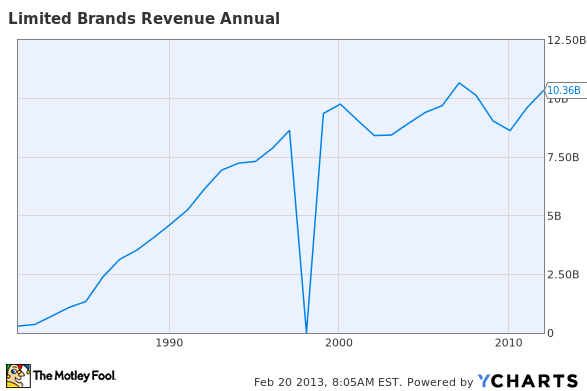

Historic revenue growth:

In 2003, L Brands Inc (NYSE:LTD) reported revenue of $8.44 billion; in 2012, the company announced revenue of $10.36 billion, representing year over year annual growth of 2.30%, a solid trend which is highly anticipated to sustain into the future with projections placing 2017 revenue at $12.68 billion (this growth has been a result of consistent product innovation and strong performance across all segments)

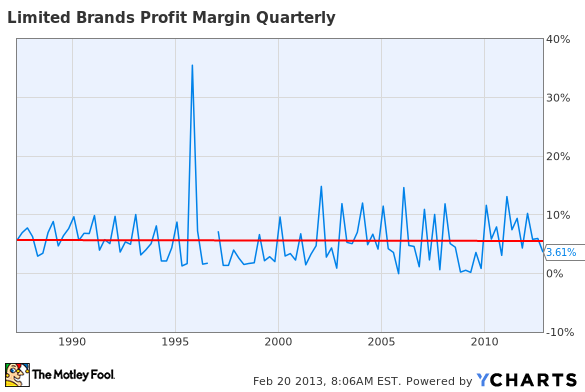

Steady profit margin:

Since 1990, L Brands Inc (NYSE:LTD)’ quarterly profit margin has gyrated around the current 3.61% level, representing a company that has performed on a consistent basis

Institutional vote of confidence:

73.68% of shares outstanding are held by institutional investors, displaying the confidence some of the largest investors in the world have in the company and its future

Strong cash flow position:

In 2012, L Brands generated $1.24 billion in cash flow, representing the financial strength of the company; this cash flow is able to support a 2.70% dividend which has a long history of growth

Reasonable valuation:

At the moment, the company carries a price to earnings ratio of 20.19 and a price to sales ratio of 1.41, both of which represent a company trading with a reasonable valuation

Weaknesses

Net debt:

The $547 million of cash and cash equivalents the company possesses on its balance sheets is outweighed by L’s $7 billion of debt, resulting in a net debt of roughly $6.5 billion, or $22.60 per share, a major financial weakness of the company

Opportunities

International expansion:

In 2011, the company launched 90 new international stores, bringing their international store count to more than 680 stores in nearly 40 countries, with $1 billion in retail sales; further aggressive international expansion is projected and provides an opportunity for the company to fuel overall growth

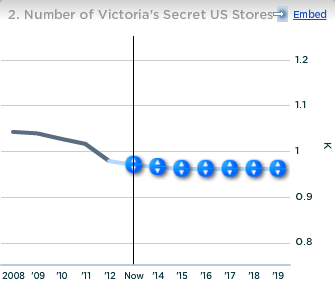

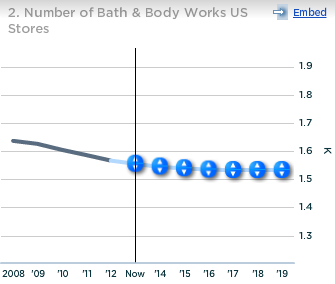

Domestically increasing store count:

In the United States, the number of Victoria’s Secret and Bath & Body stores has decreased from 1,040 K in 2008 to 970 currently, and from 1,640 in 2008 to 1,560 currently, respectively; however as economic conditions improve increasing the store count is a real opportunity

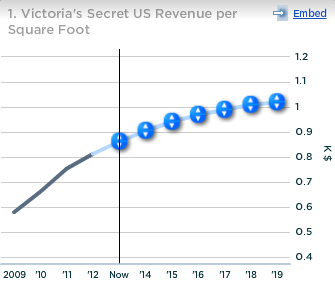

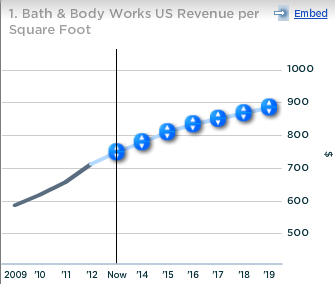

Streamlining revenue per square foot:

While over the past years total store count has been decreasing, revenue per square foot has been rising moderately (Victoria’s Secret 2009- $580 Currently- $860 Bath & Body 2009- $587 Currently- $749); with further growth in these statistics projected

Threats

Rising material prices:

L utilizes several distinct materials to compose their products, and any rise in the price of the materials the company uses could squeeze margins

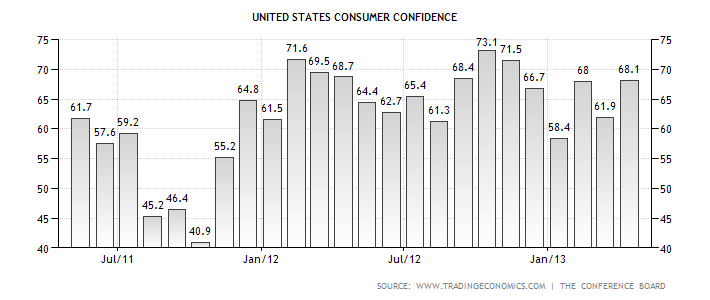

Falter in consumer confidence:

When consumer confidence prospers, customers have more conviction to purchase luxuries such as those sold at L Brands Inc (NYSE:LTD) stores, however any falter in consumer confidence could threaten sales