Dividend growth investing has become popular lately, and for good reason. The idea behind this method is to invest in companies that are likely to have strong dividend growth in the future, thus continually increasing the amount of income generated from your portfolio. This income can then be reinvested into more dividend growth stocks, creating even more income. Dividend growth investing is like compounding on steroids. Imagine you have a portfolio which generates $1,000 of dividend income each year, and that the dividends grow at 8% annually. You could either keep those dividends or reinvest them into more dividend growth stocks. What’s the difference? See the chart below.

Created with infogr.am

If you don’t reinvest your dividends over 40 years then your income stream grows to about $20,000 annually, all through the magic of compounding. But if you reinvest those dividends each year in equivalent dividend growth stocks, your income stream grows to an astounding $58,500 annually–almost three times as much! Clearly there’s an advantage to dividend growth investing.

Finding dividend growth stocks

What makes a good dividend growth stock? Well, obviously the dividend needs to be growing. But yield is important too, and just because a dividend has been growing fast doesn’t justify a sub par dividend yield. The lower the yield the higher the expected growth rate needs to be. Here are some general guidelines that I use to look for dividend growth stocks:

| Dividend yield | Required 10-year annual dividend growth rate |

|---|---|

| 2% | 14% |

| 2.5% | 11.5% |

| 3% | 9% |

| 3.5% | 7% |

| 4% | 5.5% |

| 5 % | 2.9% |

| 6% | 1.9% |

If you’re curious where these numbers come from, they’re based on a simple dividend discount model calculation, which you can easily do using my dividend valuation tool.

Projecting what the future dividend growth is going to be can be tricky. You can look to the past, but that alone can end up being deceptive. One important quantity to look at is the payout ratio, which is the percentage of profits which goes towards paying the dividend. A high dividend payout ratio, above 60% or so, usually indicates that dividend growth will come mainly from earnings growth in the future. A low payout ratio, however, allows for dividend increases to come from both earnings growth and expansion of the payout ratio.

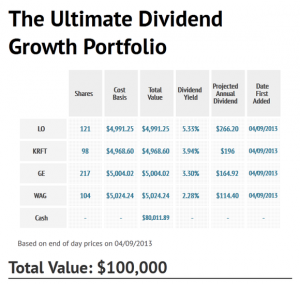

The Ultimate Dividend Growth Portfolio

In an effort to find the best dividend growth stocks today I’m introducing The Ultimate Dividend Growth Portfolio. The goal of this on-paper portfolio is to assemble a list of high-quality stocks which, through a combination of yield, exceptional dividend growth, and reinvesting dividends, provide an ever-increasing income stream. To begin the portfolio I will allocate $100,000, spread roughly evenly across 20 different positions. As time goes on the number of positions and weightings may change, but for now I’ll keep things simple. Let me introduce the first four stocks that I’ll be adding to The Ultimate Dividend Growth Portfolio.

Kraft Foods Group Inc (NASDAQ:KRFT)

Last year Kraft Foods Group Inc (NASDAQ:KRFT) split into two companies. The new Kraft Foods is focused on the North American market, while Mondelez International Inc (NASDAQ:MDLZ) operates the international brands. The North American market is fairly mature, so it stands to reason that Kraft will be a slow grower from here on out. The company’s first dividend was paid in December of 2012, and the projected yield is a hearty 3.94%. Based on my table above the dividend needs to grow at about 5.5% annually for Kraft Foods Group Inc (NASDAQ:KRFT) to be an attractive dividend growth investment.

Since the new Kraft doesn’t have much of a dividend history and looking to the past isn’t possible, the payout ratio becomes a very important metric. In 2012 Kraft generated a net income of $1.64 billion and a free cash flow of $2.60 billion. I prefer to use free cash flow when calculating the payout, ratio since it represents the actual cash that the company generated. The current $2 per year dividend will result in annual dividend payments totaling $1.19 billion, putting the payout ratio at about 46%.

The average analyst estimate for 5-year annual earnings growth is 6.3%, but since the payout ratio is fairly low, dividend growth can come from expansion of the payout ratio as well. This means that Kraft Foods Group Inc (NASDAQ:KRFT)’s dividend will most likely grow significantly faster than the 5.5% rate required by the table above. I wrote an article about Kraft last December with a little more detail, and you can read that here.

The share price as of this writing allows for 98 shares to be purchased for the portfolio, for a total cost basis of $4,968.60. The annual dividend income from this position is $196 based on the current quarterly dividend.

General Electric Company (NYSE:GE)

General Electric Company (NYSE:GE) was forced to cut its dividend during the financial crisis as its financial arm nearly ruined the company. GE’s financial position has grown stronger since then, and at the end of last year the quarterly dividend was raised by 11.7%. This puts the projected dividend yield at a healthy 3.3%.

While GE’s free cash flow has been slumping lately I don’t think that this is a long term trend. FCF for 2012 was $16.2 billion, about half of the 2008 peak, but analysts expect earnings to grow at a rate of about 11% annually for the next 5 years.

The payout ratio in 2012 was only 44%, even with the lower free cash flow, so I think that General Electric Company (NYSE:GE) will have the opportunity to raise the dividend substantially in the near future. In addition to this, CEO Jeff Immelt stated in the annual letter to shareholders that GE would be returning $18 billion to shareholders in the form of dividends and share buybacks. Share buybacks will have the effect of lowering the share count and thus decreasing the payout ratio, allowing for further future dividend expansion.

With a yield of 3.3% dividend, growth needs to be around 8% annually for the stock to be fairly priced. Given the expected earnings growth and the fairly low payout ratio I think that the dividend can grow substantially faster than this. Based on the current price I can add 217 shares of General Electric Company (NYSE:GE) to the portfolio for a total cost basis of $5,004.02. The annual dividend income from this position is $164.92, based on the current quarterly dividend.

Walgreen Company (NYSE:WAG)

Walgreen Company (NYSE:WAG) has a fairly low yield of 2.3%, which probably turns many dividend investors off from the stock. But as we’ll see, the potential for dividend growth more than makes up for it. The last time I wrote about Walgreen the stock price was about $35 per share, and since then it has run up to about $48 per share. In that article I claimed that the dividend needed to grow by about 10% annually, but now with a higher share price dividend growth needs to be closer to 12% annually.

Historically Walgreen Company (NYSE:WAG) has grown its dividend extremely quickly. From fiscal 2003 to fiscal 2012 the company grew the dividend at an annualized rate of nearly 22%, and last year it boosted the quarterly payment by 22.2%. Can this kind of dividend growth continue?

In 2012 the payout ratio was only 29%. If Walgreen raised its dividend by the required 12% per year and free cash flow remained flat it would take 5 years before the payout ratio reached 50%. And given that the average analyst estimate for earnings growth is 12.88%, a 12% dividend growth rate wouldn’t raise the payout ratio at all. I think that Walgreen can maintain its 20% dividend growth rate for quite some time going forward, making it an excellent dividend growth stock.

Based on the current share price I can add 104 shares of Walgreen Company (NYSE:WAG) to the portfolio for a total cost basis of $5,024.24. The annual dividend income from this position is $114.40, based on the current quarterly dividend.

Lorillard Inc. (NYSE:LO)

Lorillard Inc. (NYSE:LO) is the riskiest stock of the four mentioned here. First, it’s a cigarette company, and with smoking in the United States on a multi-decade decline it’s a tough business to be in. Second, Lorillard derives much of its revenue for menthol cigarettes, and it’s possible that legislation could cause problems for the company. There’s some evidence of negative health effects of smoking menthol cigarettes beyond the normal ones, so there’s always the possibility that they get banned outright.

Lorillard’s main brand, Newport, has proven to be very popular. The company has been growing revenue and earnings, and the stock offers a dividend yielding 5.33%. In a previous article I determined that Lorillard Inc. (NYSE:LO) was the best tobacco stock out there, blowing away the competition on pretty much every dividend-related metric. The dividend has grown from $0.61 annually in 2008 to $2.07 annually in 2012, an annualized rate of 35%. The payout ratio has become a bit high at about 73.6% in 2012, but for a cigarette company that doesn’t need to invest very much back into the business this seems perfectly fine.

From the table above the dividend needs to grow at about 2.5% per year, and it looks like Lorillard should have no problem with that. The company has been buying back shares as well, which should help the cause. The company’s first dividend of 2013 jumped by 6.4%, so Lorillard looks poised to deliver more than enough dividend growth in the future.

Based on the current share price I can add 121 shares of Lorillard Inc. (NYSE:LO) to the portfolio for a total cost basis of $4,991.25. The annual dividend income from this position is $266.20 based on the current quarterly dividend.

Next time

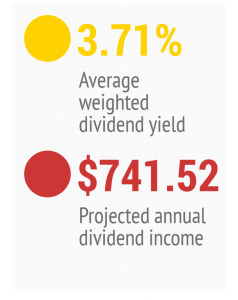

So far four of twenty stocks have been added to The Ultimate Dividend Growth Portfolio, and next time I’ll detail four more outstanding dividend growth stocks. Until then, here’s what the portfolio currently looks like.

Created with infogr.am

Timothy Green has no position in any stocks mentioned. The Motley Fool owns shares of General Electric Company (NYSE:GE).