Exxon Mobil Corporation (NYSE:XOM) has once again surpassed Apple Inc. (NASDAQ:AAPL) as the world’s most valuable company after the iPhone and iPad maker saw its stock price falter.

Apple had first overtaken Exxon Mobil Corporation (NYSE:XOM) as the world’s largest publicly traded company in August 2011, but Apple has now handed the mantle back to Exxon, following several difficult weeks which have seen its share price fall to a 12 month low. Apple as of now has a total market cap of $413.06 billion; Exxon, on the other hand, has a market cap of $418.23 billion.

Exploration projects can take years to yield new production. And some of Exxon’s biggest investments recently have been in U.S. natural gas fields, which so far haven’t paid off because prices have dropped to their lowest levels in a decade. Crude production declined as some of its fields matured and produced less. And many contracts in foreign countries limit the amount of oil that Exxon can sell as prices rise, not to mention the fact that natural gas demand fell in Europe as well.

Overall, earnings in Exxon’s exploration and production business rose 18 percent, offsetting a 63 percent drop in income from the company’s refining business. The company’s refineries, which produce gasoline, diesel, and other fuels, have struggled to pass on the higher cost of their primary input, which is crude. Exxon announced that it is selling its Japanese refining and marketing business for $3.9 billion following an extended slide in Japanese fuel demand. Exxon’s chemicals business also saw profits decline 49 percent. For the full year, Exxon’s net income rose 34.8 percent, while revenue rose 26.9 percent.

Since mid 2010 Exxon’s market price has increased from its low of about $57 to the current price of about $91 per share, as is shown in the graph below. That is an increase of 60% in market price in 2.5 years time. Also it is interesting to see that it is back around its pre-crisis high.

Source: Ycharts.com ( X-axis: Year, Y-axis: Share Price)

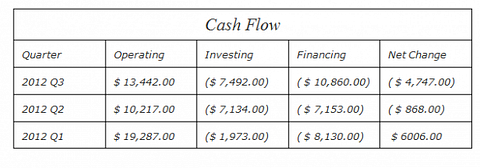

An intensive analysis of Exxon’s cash flow statement highlighted one strong point of Exxon–the ability to generate huge amounts of cash.

Operating cash indicates if the company is able to generate its own cash, instead of funds coming from outside financing activities. As shown in the tables below, operating cash is growing year over year as of 2009, with a slight decrease in 2012.

With operating cash the company is able to fund its investing and financing requirements. As we look at the increase/decrease in net cash in the tables, we see that Exxon has significantly been using up its cash reserves in the last few quarters. One of the main reasons is that it has been buying back its own stock–already about 15.6 billion worth in 2012. In a cash flow statement this is indicated with the “Issuance (Retirement) of Stock, Net” item.

Note: All values in tables are in Millions of USD

Exxon vs Other Companies

Major oil companies’ fourth-quarter earnings reports got off to a bumpy start, with Royal Dutch Shell plc (ADR) (NYSE:RDS.A)’s profit disappointing investors and ConocoPhillips (NYSE:COP) projecting total production for this year will be lower than in 2012.

ConocoPhillips, based in Houston, said that because of planned maintenance, downtime at some facilities, and seasonal issues in the second and third quarters of 2013, it expects full-year production from continuing operations of 1.48 million to 1.53 million barrels of oil equivalent per day. Full-year 2012 production was 1.58 million barrels per day. The muted outlook came as the company reported that its fourth-quarter profit fell nearly 58 percent. The decline partly reflected the spinoff of downstream businesses that were included in the year-ago results. The spinoff of the new Phillips 66 removed ConocoPhillips from the ranks of integrated, Big Oil rivals, against which it’s been measured in the past.

ConocoPhillips earned $1.43 billion, or $1.16 a share, in the final three months of 2012, compared to a profit of $3.39 billion, or $2.56 a share, for the same period a year earlier when results included earnings from the spun-off downstream businesses. Excluding one-time items, fourth-quarter adjusted earnings were $1.43 per share. Revenue for the period was $16.4 billion, compared with $16.1 billion a year earlier. For all of 2012, the company earned $8.43 billion, or $6.72 a share, compared with full-year 2011 earnings of $12.44 billion, or $8.97 a share. The 2011 profit included 12 months of downstream earnings, and the 2012 figure included the four months of combined earnings before the spinoff of the new Phillips 66.

Royal Dutch Shell, based in the Netherlands with its U.S. headquarters in Houston, posted a 2.6 percent rise in fourth-quarter net earnings. The results fell short of expectations. Its production rose in the fourth quarter, but expense,s including its problem-plagued initial foray into Alaskan Arctic waters, took a toll on the bottom line. It plans to continue with its aggressive investment programs in the year ahead.

The company reported $6.67 billion in fourth-quarter profit, or $1.06 a share, compared with a profit of $6.5 billion, or $1.04 a share, in the same period the previous year. Revenue in the quarter was $118.05 billion, compared with $115.58 billion in the year-ago quarter. Shell earned $26.59 billion, or $4.24 a share, in 2012, compared with $30.92 billion, or $4.97 a share, in 2011. Twelve-month revenue came to $467.15 billion, compared with $470.17 billion in 2011. Shell plans to use ambitious exploration strategies to achieve its goals, and has spent more than $5 billion on its Arctic exploration activities.

Conclusion

In comparison to Conocophillips and Royal Dutch Shell, I believe that ExxonMobil is the world’s best-run integrated oil company, based on its track record of superior returns on capital. The company boasts diversified operations across the world, with several new projects coming online through 2013.

The company’s efforts to build an unconventional resource portfolio both in North America and overseas aims at increasing production through increased exposure to large energy resources with long reserve life and low field declines. Despite the collapse in natural gas prices, ExxonMobil expects unconventional gas to play a dominant role in future supplies, owing to the rapid decline in conventional production. Its strength lies in its balanced operations, strong financial flexibility, and continuous improvement on efficiency and cost control.

With the energy sector acting as a defining catalyst for economic growth, Exxon is a good investment at its current price.

The article Exxon Mobil- What the Numbers Say originally appeared on Fool.com and is written by aakanksha patodia.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.