PPG Industries, Inc. (NYSE:PPG) may not be a household name for dividend investors, but it has an impressive company history. It was founded in 1883, as Pittsburgh Plate Glass.

Today, PPG operates across the world, with 47,000 employees and nearly $15 billion in annual sales.

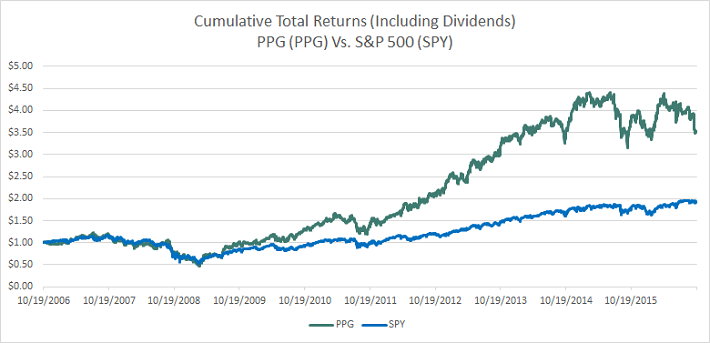

PPG stock has delivered a 245% total return to shareholders over the past decade.

The stock offers steady earnings growth and a long track record of paying dividends. In fact, PPG has paid (1) 472 consecutive quarterly dividends, and has made uninterrupted dividend payments… since 1899.

PPG has increased its dividend for 44 consecutive years. The company’s long dividend streak makes it a member of the exclusive Dividend Aristocrats. There are currently just 50 businesses that meet the criteria to be in this index:

– 25+ years of consecutive dividend increases

– Be a member of the S&P 500

You can see all 50 Dividend Aristocrats here. PPG’s quarterly dividend history since 1983 is shown below for a graphical representation of its history of dividend increases.

PPG is not the highest yielding stock. It’s dividend yield is currently a lackluster 1.7%. What the company lacks in yield, it has historically made up for in growth.

Keep reading to learn more about the investment prospects of PPG.

Business Overview

PPG is a global supplier of paints, coatings, optical products, specialty materials, and fiber glass. It services a wide range of end users, including the industrial, transportation, consumer products, and construction industries. Its products are used primarily to enhance surfaces.

Going forward, PPG intends to focus on paints and coatings. To do this, it has divested low-margin businesses and significantly reduced its presence in glass and chemicals. It has also made several acquisitions—6 acquisitions last year alone that added $400 million in annual revenue—to further expand into coatings.

Source: 2016 Investor Overview, slide 8

Follow Ppg Industries Inc (NYSE:PPG)

Follow Ppg Industries Inc (NYSE:PPG)

Receive real-time insider trading and news alerts

PPG will derive 96% of its net sales each year from coatings. Previously, it collected 55% of its sales from coatings. PPG’s streamlined business model should propel further revenue growth and margin expansion.

Growth Prospects

PPG Industries, Inc. (NYSE:PPG) maintains a focused strategy because it believes paints and coatings will have the highest growth potential in the future. This should be a beneficial strategy, since the coatings business has grown profit at an 11% compound annual rate over the past decade.

PPG also has a proven track record of successfully generating growth from mergers and acquisitions.

Source: 2016 Investor Overview, slide 10

PPG should be able to pursue additional growth opportunities, as the company ended last quarter with $1.7 billion in cash and cash equivalents on hand. This cash can be used for future bolt-on acquisitions to drive earnings growth.

Another positive aspect of PPG’s portfolio restructuring is that the company will have a much bigger presence in the international markets, particularly the emerging markets like China. This should boost earnings growth because demand from the emerging markets is likely to grow at a higher rate than in the U.S.

Source: 2016 Investor Overview, slide 12

Last year, 55% of the company’s net sales came from outside the U.S. and Canada. Approximately 26% of total revenue was derived from emerging markets. Compare this with one decade earlier, when the U.S. and Canada comprised 72% of PPG’s total revenue.

The benefits of this strategy are already being felt. Earnings-per-share, as adjusted for divestitures and one-time financial items, increased 14% last year.

PPG is performing well to start 2016. Adjusted earnings-per-share rose (2) 11% in the second quarter. Last quarter was its 14th in a row of double-digit adjusted earnings-per-share growth.

PPG should also realize earnings growth from its share repurchase program. The company utilized $750 million in share buybacks last year. It can return cash to shareholders through dividends and buybacks because it generates significant cash flow. Last year, PPG’s cash flow from operations reached a record $1.8 billion.

Share buybacks help grow earnings-per-share because fewer shares outstanding receive a larger portion of a company’s earnings-per-share, thus making each share more valuable.

Competitive Advantages & Recession Performance

The paint industry has very favorable economics. It has high margins and requires little capital investment. It generates a lot of cash. PPG clearly has a strong and durable competitive advantage in this high margin industry. It’s 4 decade (and counting) dividend streak is evidence.

PPG Industries has the highest margins in the industry of any major player. Its high margins helped the company remain profitable during the Great Recession.

– 2007 earnings-per-share of $5.03

– 2008 earnings-per-share of $3.25

– 2009 earnings-per-share of $2.03

– 2010 earnings-per-share of $4.63

– 2011 earnings-per-share of $6.87

The recession clearly did a lot of damage to PPG, as it is exposed to the real estate market. When less buildings and houses are build, less paint is sold. People also tend to hold off on doing cosmetic home repairs when money is tight.

But PPG bounced back very quickly. The company has benefited from the steady economic recovery since 2009. Over the past decade, PPG has increased earnings-per-share and dividends by 11.4% and 4.3% per year, respectively.

Valuation & Expected Total Return

PPG stock trades for a price-to-earnings ratio of 17.2. By comparison, the S&P 500 Index has a price-to-earnings ratio of 24.

The company will likely grow future earnings in the high single-digit range, so a market multiple seems appropriate. This could indicate the stock is undervalued.

PPG has a current dividend yield of 1.7%. It should be able to increase dividends at a double-digit rate going forward, in line with its 11% dividend increase in 2016. The main reasons for this are projected earnings-per-share growth, plus PPG has a low payout ratio. PPG’s forward annualized $1.60 per share dividend represents 30% of its trailing 12 month earnings-per-share. This is a modest payout ratio that leaves plenty of room for generous dividend raises.

The combination of earnings growth and the dividend yield could reach double-digit annualized returns for investors going forward.

It should be noted that PPG’s returns are ‘lumpy’. The company does not grow the same amount every year. PPG sees earnings-per-share (and typically its share price) fall significantly during recessions. When the economy isn’t in recession, PPG tends to grow quickly.

Final Thoughts

PPG Industries, Inc. (NYSE:PPG) stock has a below-average dividend yield, which may not make it a compelling buy for investors who desire current income. However, dividend growth investors (3) may view the stock more attractively.

The company is poised to grow earnings-per-share at a strong rate moving forward, as it benefits from increasing consumer demand in the U.S. and internationally.

As a result, its double-digit dividend growth rate potential makes it an appealing stock for dividend growth investors with longer investing time horizons. The company currently ranks very well using The 8 Rules of Dividend Investing thanks to its low payout ratio, reasonable valuation, and strong expected long-term return potential.

Note: This article is written by Bob Ciura and was originally published at Sure Dividend.

Additional Links:

(1) http://investor.ppg.com/press-releases/2016/07-21-2016-150214736

(2) http://investor.ppg.com/press-releases/2016/07-21-2016-115113548

(3) http://www.suredividend.com/11-reasons-to-be-a-dividend-growth-investor?utm_source=bc&utm_medium=sd&utm_campaign=101916sd2