![]()

Church & Dwight Co., Inc. (NYSE:CHD) was founded more than 160 years ago, but still remains relatively unknown or ignored by most investors. The company generates $3 billion in annual sales via brands such as Arm & Hammer, OxiClean, Trojan, and First Response. The market capitalization currently sits at just under $9 billion, much less than larger peers, and it is generally viewed as a mid-cap.

Strong, consistent earnings growth

What makes the stock such a strong candidate for those swapping out of bonds is the top-notch consistency in the company’s results. They have generated earnings-per-share growth of at least 10% for twelve consecutive years! This is rare class indeed. The worst recession in seventy years, which clobbered most company’s results, did little to Church & Dwight Co., Inc. (NYSE:CHD)’s performance. The Procter & Gamble Company (NYSE:PG) is the bellwether in the consumer products space and still a relatively safe option from a return of capital standpoint. But the company is subpar operationally with just 4% CAGR in operating EPS over the last five years whereas Church & Dwight is four times higher at 12%.

Colgate isn’t a bad investment option for conservative investors thanks to above-average organic sales growth that is a byproduct of dominating their oral care franchise. While Colgate is a good investment option for conservative investors looking to increase equity exposure, especially relative to The Procter & Gamble Company (NYSE:PG), Church & Dwight Co., Inc. (NYSE:CHD) is likely a better option. Colgate has already made their big international push and generates less than 20% of earnings from North America. Conversely, Church & Dwight Co., Inc. (NYSE:CHD) generates more than 75% of earnings from North America. They have a long-tail on their international growth opportunities.

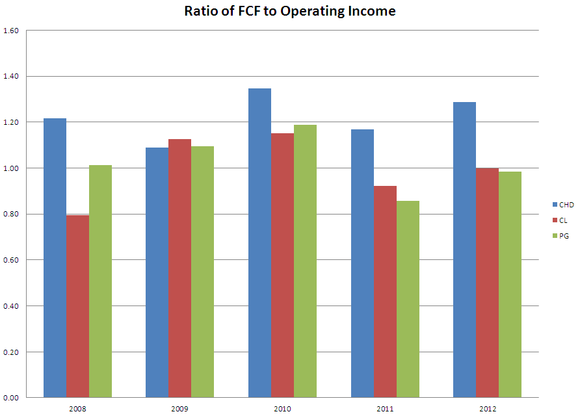

Church & Dwight Co., Inc. (NYSE:CHD) also has higher quality earnings. This can be measured by looking at free cash flow divided by net income. A higher ratio indicates strength in earnings with high cash conversion and less accounting gimmicks.

Magnificent management

Church & Dwight Co., Inc. (NYSE:CHD)’s success stems from operating in industries with steady demand drivers, but also in the ability of management to consistently drive margins higher.

CHD Operating Margin TTM data by YCharts

Why have margins done so well? Part of this has to do with declining interest expense, something that all companies have benefited from. But Church & Dwight has little debt, making them a good candidate where safety of capital is a priority, so this is only a little part. Much has to do with management knowing how to run a business in an optimal way. This includes focusing on the key brands, of which the company identifies eight, and driving market share gains. The company has a good split of premium and value brands, which has also been crucial as frugal consumers continue to shift to value brands. Investors can feel confident that management is driving the ship in the right direction.

Increasing margins isn’t easy to do either as several peers have seen little change during the last decade.

PG Operating Margin TTM data by YCharts

The Foolish Bottom Line

Church & Dwight Co., Inc. (NYSE:CHD) makes for an ideal equity swap for investors looking to reduce their fixed income exposure. The company is small enough to maintain its laser-like focus on key brands but has the size and stability to generate some of the most consistent results among all public companies. The stock trades at a 5% premium to Colgate and a 20% premium to The Procter & Gamble Company (NYSE:PG) using P/E ratios, but it is growing at ratios much higher. Buying now seems like a near certainty to yield 10-year total returns well in excess of investment grade bonds. Waiting for a modest pullback would only enhance the stock’s total return potential.

The article Would You Rather Own Bonds or This Stock? originally appeared on Fool.com and is written by Justin Carley.

Justin Carley has no position in any stocks mentioned. The Motley Fool recommends Procter & Gamble. Justin is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.