It has been a rough 2013 for Apple investors. While the Dow Jones Industrial Average has climbed 12.60%, Apple Inc. (NASDAQ:AAPL) has declined -24.48%. The 2013 year has been marked with a disappointing earnings report, an apparent lack of innovation, and a flurry of analyst downgrades, all of which have contributed to the share price seen today. With the company trading at levels not seen since 2011, is it finally the right time for investors to take a bite out of Apple?

Core Business Fundamentals

What?

Apple Inc. (NASDAQ:AAPL) “designs, manufactures and markets mobile communication and media devices, personal computers, and portable digital music players, and sells a variety of related software, services, peripherals, networking solutions, and third-party digital content and applications.” The company’s product portfolio includes the iPhone, iPad, Mac, iPod, Apple TV, a portfolio of consumer and professional software applications, the iOS and OS X operating systems, iCloud, and a variety of accessory, service and support offerings.

In 2012, the iPhone segment accounted for 51.41% of overall revenue, iPad segment represented 20.72% of overall inflow, the Mac segment translated into 14.84% of overall revenue, and the remaining 13.03% was allocated in the music related products and services, iPod, software, and peripheral segments.

How?

“Apple Inc. (NASDAQ:AAPL) sells and delivers digital content and applications through the iTunes Store, App Store, iBookstore, and Mac App Store. The company sells its products worldwide through its retail stores, online stores, and direct sales force, as well as through third-party cellular network carriers, wholesalers, retailers, and value-added resellers.”

Where?

The geographical breakdown of the company’s revenue in 2012 was split 38.95% United States, 14.56% China, and 46.49% other countries.

Profitability Metrics

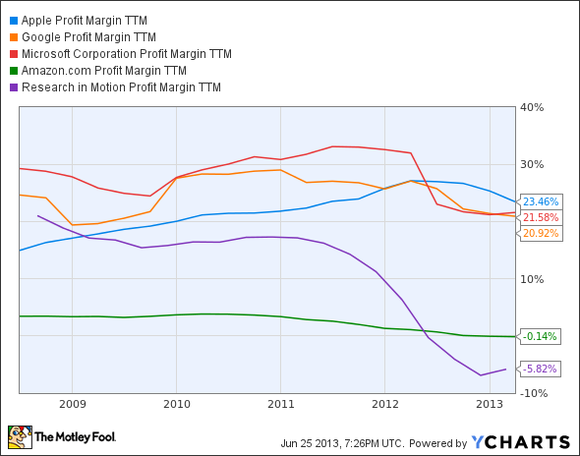

All of the company’s profitability metrics (TTM profit margin, return on equity, return on assets) are relatively strong and in the double digits, however these percentages have been sharply declining since the beginning of 2012 and are projected to continue to decline through 2017 as increased competition and rising costs tighten the company’s profit.

TTM profit margin “Measures how much out of every dollar of sales a company actually keeps in earnings” (Source: Investopedia).

With the largest profit margin in the industry, Apple Inc. (NASDAQ:AAPL) is able to retain more revenue as earnings, a crucial advantage. The company’s immense brand loyalty and pricing power has allowed the company to grow its profit margin over the past set of years, however projections display the margin faltering as competition mounts, which could lead to slight earnings deterioration by 2017.

Risk Assessment

The risk associated with Apple Inc. (NASDAQ:AAPL) as an investment can be classified as high, as they operate in an ever-evolving market for technological products in which consumer’s desires are constantly changing. The potential slowed pace of innovation stemming from the alteration in the company’s management after the death of the legendary founder, Steve Jobs, also contributes to this risk assessment.

Valuation

Presently, Apple possesses a price to earnings ratio of 9.65 and a price to book ratio of 2.80, both of which are five year lows for the company.

Considering that revenue is anticipated to grow at a high single-digit rate through 2017 and that earnings are projected to grow at a mid-single digit rate until 2015, and then reverse course and decline to the current levels by 2017, the valuation of Apple is severely depreciated. As the S&P 500 currently carries a price to earnings ratio of 16.15 and a price to book ratio of 2.27, and the estimated rate of growth of the S&P 500 is subpar in terms of revenue and in-line in terms of earnings compared to that projected for Apple, Apple’s valuation can only be classified as undervalued. If Apple was awarded the same price to earnings ratio as the S&P 500, the price of a share would rise to $676, representing approximately 69% upside from current levels.