Valuing Tesla in January 2020

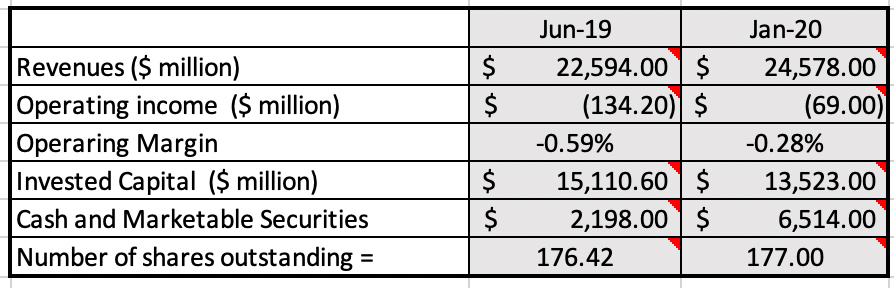

There have been three earnings reports from Tesla Inc (NASDAQ: TSLA) since my June 2019 report, and the table below shows how the base year numbers have shifted, as a consequence:

|

| Tesla Quarterly Reports & Earnings Call on January 29, 2020 |

The base revenues have increased by about 9%, and operating margins continued to get less negative (turning positive in the last quarter of the year), as long-promised economies of scale finally manifested themselves. In the table below, I highlight the changes that I have made in key inputs relating to growth, profitability and reinvestment.

|

| Download spreadsheet |

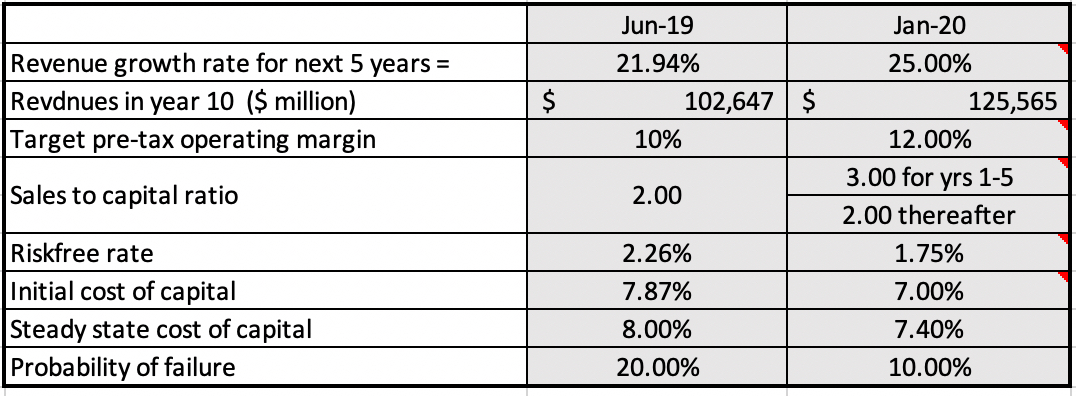

Specifically, here is what I changed:

– Higher end revenues: My revenue growth rate, while only marginally higher than the growth rate I used in June 2019, delivers revenues of just above $125 billion in 2030, about 25% higher than the end revenues that I forecast a year ago. Since this will require that Tesla sell more than 2 million cars in 2030, I am not making this assumption lightly.- Higher margins: My target pre-tax operating margin has also been pushed up from 10% to 12%, reflecting the improvements in margins that the company has already delivered and an expectation that the company will continue to work on a more efficient production model than conventional automakers.- More efficient reinvestment: My reinvestment assumptions for the long term resemble those that I made in June, with every dollar in invested capital delivering $2 in revenues, as the company adds capacity. In the near term, though, I assume less reinvestment, assuming $3 in revenues for every new dollar of capital invested, since Tesla contends in its January 2020 earnings call to have capacity online to produce 640,000 cars, enough to cover growth for the next year or two.

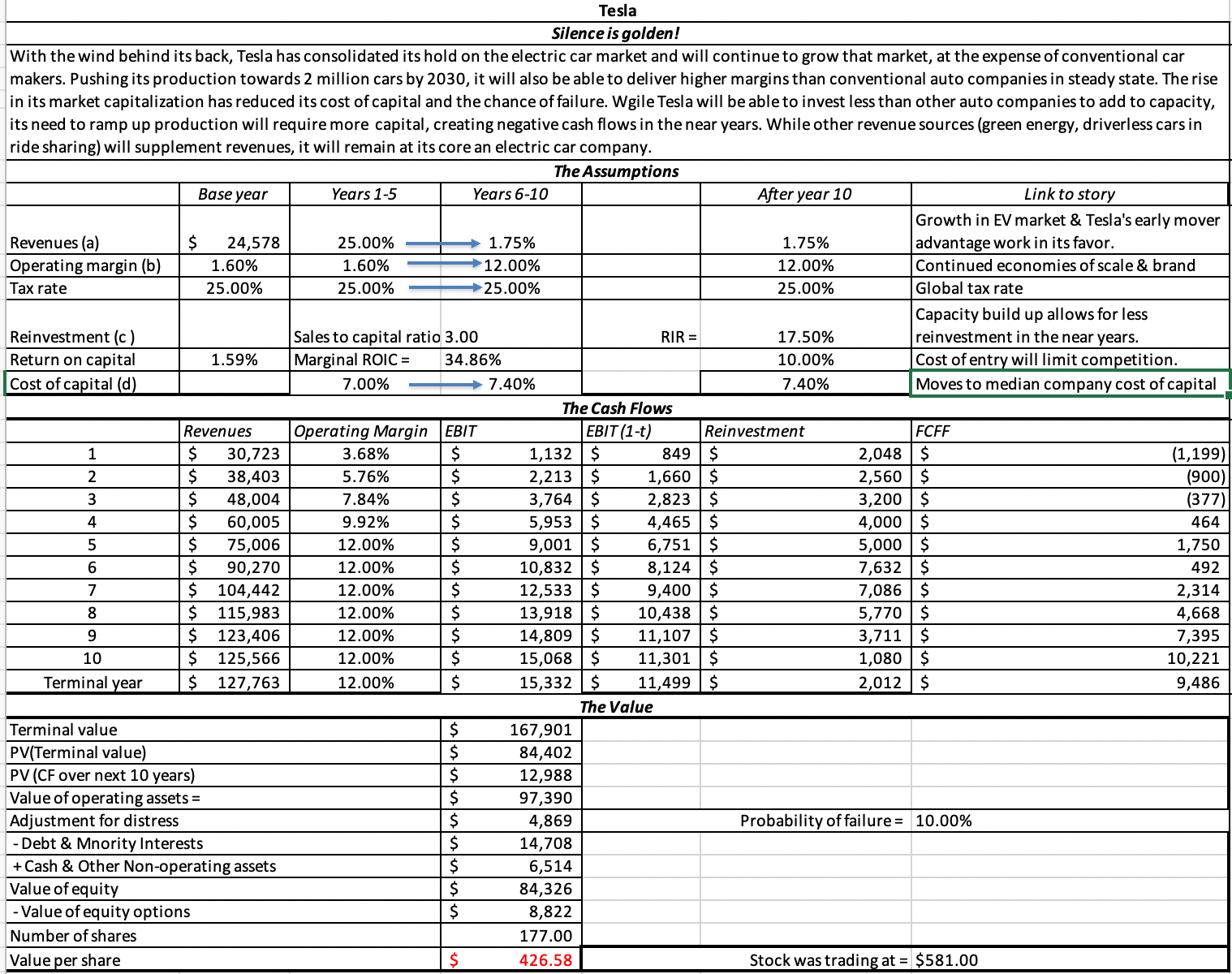

If you are surprised about the lower cost of capital in January 2020, that drop has little to do with Tesla and more to do with changes in the market. First, the US treasury bond rate has dropped to 1.75% from 2.26% in June 2019, creating a lower base for both the costs of equity and debt for the company. Second, while Tesla’s bond rating has not improved dramatically, default spreads on bonds have dropped over the course of the year. Finally, the price feedback effect has silenced talk about imminent default, but I understand that a momentum shift and a lower stock price can rekindle it, and I have halved the probability of default. With this more upbeat story, the value that I get per share for Tesla is $427, and the details are shown below:

|

| Download spreadsheet |

If your criticism of this valuation is that I am letting the good times in the stock feed into my intrinsic value estimate, I am guilty as charged, but I have never been able to completely ignore what markets are doing, when doing intrinsic value. To see how each assumption that I have altered feeds into the value, I broke down the value change into constituent pieces.