Acuity Brands’ secular growth drivers

The decreasing cost (per lumen) of LEDs means that Acuity can generate growth from LED lighting replacing conventional lighting. Margins on LED lighting are similar to conventional bulbs, but Acuity argues that it sells controls with virtually all its LED lights. Lighting controls are an essential part of the value proposition because, they help to increase the efficiency of lighting solutions.

The good news is that this is driving sales growth. Its net sales were up 11% in the third quarter, as opposed to the ‘low single digit growth rates’ that it claims its markets are growing at. The ‘bad’ news is that volumes grew by 14%. The discrepancy is due to lower prices of LED components and an unfavorable product mix. Essentially, Acuity Brands, Inc. (NYSE:AYI) is providing relatively more solutions to lower margin renovation work because large scale new construction hasn’t kicked in yet thanks to the slow economy.

Acuity’s LED-based revenue is now at 20% of its total, from 15% and 13% in the previous two quarters. This is a powerful trend.

For example, a company like Cree, Inc. (NASDAQ:CREE) is more of a pure LED play than Acuity. It offers a vertically integrated way to play growth in LEDs. Lighting looks set to be the primary driver of the next upswing in the LED cycle. Cree’s own lighting division managed to increase sales by 6% in the last quarter, even with unseasonal weather negatively affecting outdoor lighting sales.

Cree’s lighting products gross margins are at 30.6%, while Acuity Brands, Inc. (NYSE:AYI)’s numbers are at a more impressive 40.8%. Acuity has a more mature sales operation, while Cree uses sales agents. Nevertheless, Cree appears to have the opportunity to improve its lighting products margins going forward. Cree’s lighting product revenues currently represent nearly 38% of its total, so the opportunity is significant.

Cyclical growth drivers

Acuity can see cyclical growth in two ways. The first is from a general pickup in construction activity, and the second is through margin expansion, as more profitable activity like large-scale new construction takes place. Historically speaking, the former usually entails the latter.

In addition, investors need to appreciate that lighting is one of last phases of construction, so a natural time lag exists between general activity and orders coming in for lighting.

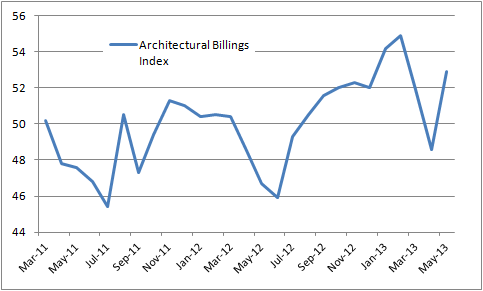

All eyes will be fixed on construction indicators such as the Architectural Billings Index (ABI) from the American Institute of Architects. It has been unusually volatile lately.

One explanation for this is the late spring this year, plus delays over worries with issues like the sequester and payroll taxes.

Moreover there are some peculiar recent dynamics which can be seen in the ABI data.

The recent weakness in the commercial/industrial (C & I) sector is concerning because it’s Acuity’s strongest end market. The hope is that new residential construction will feed into new C & I construction as infrastructure is built up around the new housing. Unfortunately, it hasn’t happened yet.

Other companies have talked of weakness. REGAL-BELOIT CORPORATION (NYSE:RBC) revealed a shocker of an earnings announcement at the end of April. The company makes the kinds of motors used in heating, ventilation and air conditioning systems.

Regal lost a major contract when a customer decided to source components from a third party (rather than buy from Regal Beloit and manufacture themselves) and, overall its commentary on its C & I markets was poor. Guidance was lowered and, the strength that it had seen in January fell away through the quarter. The ABI data has weakened since then so it’s anybody’s guess what it will say in its next set of results. On the other hand, it’s cheap on a cash flow basis and, this could be a decent entry point.

The bottom line

In conclusion, you need to believe in both these drivers to want to buy Acuity Brands, Inc. (NYSE:AYI) at this level. While secular growth looks assured, it is far from clear that the cyclical growth is. On a trailing PE ratio of nearly 32, compared to its smaller rival Hubbell at 20, the stock is not cheap. I share some of the optimism over this company, but a strong and sustained recovery in the C & I market is not a “done deal.” That makes Acuity one for the monitor list.

The article Can This Stock Keep Lighting Up Your Portfolio? originally appeared on Fool.com and is written by Lee Samaha.

Lee Samaha has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Lee is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.