Earnings reports can make or break a stock. With the market near all time highs, we have to choose wisely if we are going to make a play. I have my eye on three companies this week; one is worth buying, one is worth holding, and the other is one to avoid.

“The Service Professionals”

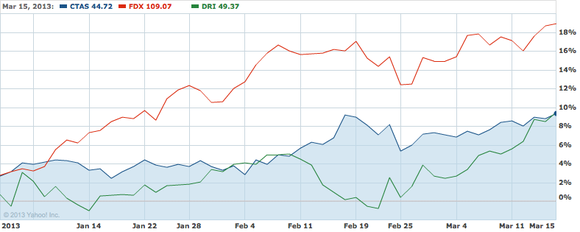

Cintas Corporation (NASDAQ:CTAS), the largest uniform company in the United States, reports third quarter earnings on Tuesday. Other than uniforms, they provide document management, cleaning services, fire protection, and safety products. The strong employment numbers we have seen over the last few months will drive demand for these services. For example, as companies add employees, they need more uniforms and apparel to outfit them. Analysts currently expect earnings per share to come in at $0.61, but I believe this is much too low.

Earnings were $0.60 and $0.63 per share for the first and second quarters, respectively, which are increases of 15.4% and 10.5% year-over-year, respectively. The $0.61 expected for this quarter is only a 5.2% increase. I believe the trend of 10%+ growth will continue, so earnings of $0.64 to $0.66 is more likely. I also believe they will exceed the $1.06 billion revenue estimate and be more in the area of $1.10 billion. If all goes as planned, Cintas Corporation (NASDAQ:CTAS) should push above the $48 mark. I want to buy this stock on any weakness.

Federal Express

On Wednesday, the market will hear from FedEx Corporation (NYSE:FDX). This shipping giant’s stock is up nearly 20% over the last 3 months, so even a blowout quarter may only move the stock a little bit. Current estimates are calling for earnings per share of $1.39 on revenue of $10.85 billion.

Earnings of $1.39 would be a 10.3% decline year-over-year, making it three straight quarters of decreases. This is mainly due to decreased shipment volumes in Europe as their economy continues to struggle. Revenues of $10.85 billion would be a 3% increase. Although this looks like a disappointing quarter, I think investors are buying for full year 2013 and 2014 expectations. Earnings are expected to be on the rise, so a few hiccups here and there won’t deter people from continuing to pile in. If you currently own the stock I would hold onto it, but I would not buy more ahead of the report. I would wait for a pull back of 5%-10% to buy.

Problems in the Restaurant Biz

Darden Restaurants, Inc. (NYSE:DRI), the owner of Olive Garden, Red Lobster, and other restaurants, will report third quarter earnings on Friday. This company has had major problems increasing customer traffic and yet the stock has risen over 9% in the last 30 days. Same store sales have declined in December and January, and are expected to fall another 4.5% in February. Analysts are currently estimating earnings to be $1.01 on revenue of around $2.3 billion.

The company’s second quarter earnings fell 37%, and the estimated $1.01 for the third quarter will represent a 19.2% decrease year-over-year. $2.3 billion in revenue would be a 4.5% growth from the previous year, a very unimpressive number. With earnings expected to drop another 10% in the fourth quarter, I think Darden Restaurants, Inc. (NYSE:DRI)’s run is over, and the company will head lower. I would sell this stock immediately and wait to buy until their yield rises to 4.75%.

The Foolish Bottom Line

February housing starts data and a Federal Reserve meeting will also be taking place this week. Keep an eye on these events, as they will have a strong influence on the direction of the market. Again, I am looking to buy Cintas, hold FedEx Corporation (NYSE:FDX), and avoid Darden.

The article 3 Stocks to Watch This Week originally appeared on Fool.com and is written by Joseph Solitro.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.