For 1Q, RadioShack posted a $0.35 loss on 5.7% lower same-store sales and 7% lower total sales. Going forward, the pressures still appear to be afoot, as the retailer ended its partnership with Target Corporation (NYSE:TGT) for providing mobile kiosks in its stores.

RadioShack Corporation (NYSE:RSH) is now looking to increase its exposure to the smartphone market, which will structurally pressure gross margins. However, the competition is rich there too, with Best Buy Co., Inc. (NYSE:BBY) breaking into the market. Best Buy has opened 525 Samsung Experience shops in its big-box stores nationwide and another 390 in its smaller Best Buy Mobile stores.

Best Buy posted EPS of $0.32 compared to $0.76 for the same period last year; this beat consensus forecasts of $0.26. The earnings beat has in part lifted Best Buy’s stock of late, yet, a bigger problem is contracting margins; gross margin contracted 60 basis points to 22.6% last quarter year-over-year, and operating margin was down 170 basis points to 5.5%.

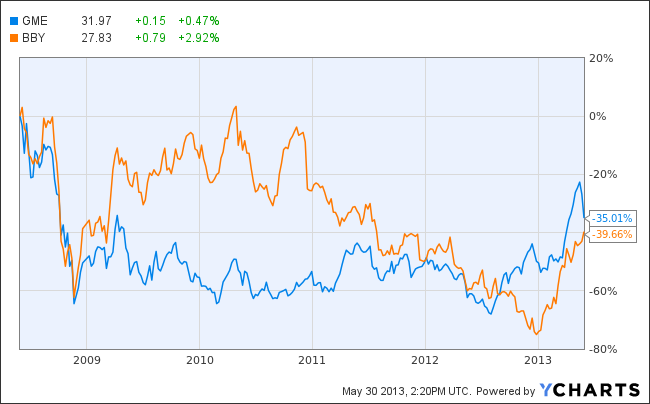

Best Buy has seen a nice rebound; yet, I would argue that Best Buy should not outperform GameStop Corp. (NYSE:GME), and both should not be trading so closely on a long-term horizon. Over the past five years, both are down between 35% and 40%.

The numbers game

So why should GameStop outperform Best Buy? Well, for one, GameStop pays a dividend yield that’s 100 basis points higher than that of Best Buy:

| GameStop | Best Buy | |

|---|---|---|

| Dividend yield | 3.5% | 2.5% |

| GameStop | Best Buy | RadioShack | |

|---|---|---|---|

| EBITDA Margin | 9.0% | 4.5% | 0.7% |

| Debt to Capital | 0.0% | 37.0% | 56.0% |

Yet, GameStop still lacks the respect it deserves. GameStop trades at a lower forward P/E multiple than Best Buy, but its expected growth is much more robust.

| GameStop | Best Buy | |

|---|---|---|

| Forward P/E | 8.7 | 11.5 |

| 5-Yr. Expected EPS Growth | 10.0% | 3.3% |

Bottom line

GameStop no doubt has uncertainty related to the specifics on how the console makers plan to offer games, whether it be a move toward more digital or the prevention of sharing hard-packaged games. However, I think the recent sell-off is an overreaction. RadioShack and Best Buy are currently battling each other in a race to mobile, leaving GameStop Corp. (NYSE:GME) as the premier company for gaming.

Given GameStop’s current dividend yield and valuation, I think the downside is limited. In addressing the 25% of sales from used games, even if we assume fiscal 2015 EPS (January 2015) comes in 20% below analyst estimates at a P/E ratio of 11.5, GameStop would still manage to trade at current levels in 21 months.

The article What Will Stop GameStop? originally appeared on Fool.com and is written by Marshall Hargrave.

Marshall Hargrave has no position in any stocks mentioned. The Motley Fool owns shares of GameStop and RadioShack. Marshall is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.