The Dow Jones Industrial Average is down following some mixed economic reports and yesterday’s release of the minutes of the Federal Reserve’s January Open Market Committee meeting. As of 1:15 p.m. EST the Dow is down 77 points, or 0.55%, to 13,850. The S&P 500 is down 0.75% to 1,500.

There were five U.S. economic releases today.

| Report | Period | Result | Previous |

|---|---|---|---|

| Initial unemployment claims | Feb. 9 to Feb. 16 | 362,000 | 342,000 |

| Consumer Price Index | January | 0% | 0% |

| Core CPI | January | 0.3% | 0.1% |

| Markit flash U.S. PMI | February | 55.2 | 55.8 |

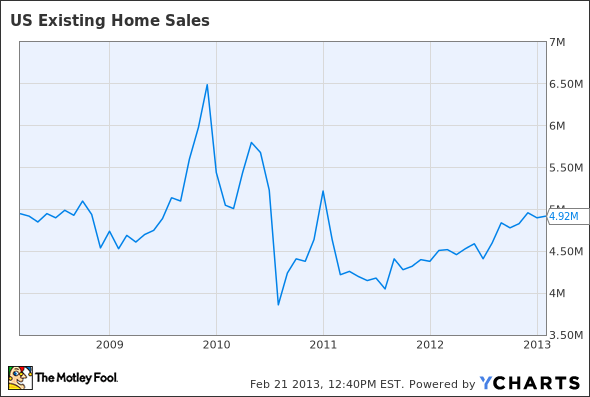

| Existing-home sales | January | 4.92 million | 4.90 million |

| Leading Indicators | January | 0.2% | 0.5% |

Source: MarketWatch U.S. Economic Calendar.

This morning the Department of Labor reported that the level of new unemployment claims rose to 362,000. That’s above last week’s 342,000 and above analyst expectations of 351,000. The four-week moving average rose to 360,750, up from 352,750. The four-week moving average is a less volatile measure of the level of new unemployment claims. New unemployment claims were basically flat through 2012 around the 360,000 to 370,000 level.

US Initial Claims for Unemployment Insurance data by YCharts.

The second economic release also came from the Department of Labor, which reported that the Consumer Price Index was unchanged in January. Economists were expecting a slight rise of 0.1%. Over the past 12 months, the CPI is up 1.6%. Food prices were flat, while energy prices fell in January. Core CPI, which excludes the volatile food and energy categories (because, really, who uses those?), rose 0.3%. That was above analyst expectations of a 0.2% rise and above December’s 0.1% growth.

The third economic release was from Markit, which reported that its flash U.S. Purchasing Managers Index fell to 55.2 in January. A PMI greater than 50 signals growth, 50 signals no growth, and anything lower than 50 signals contraction. While the PMI dropped by 0.6, a level of 55.2 still signals growth — just at a slower rate than in the previous month.

The fourth economic release was from the National Association of Realtors, which reported that existing-home sales increased to a seasonally adjusted annual rate of 4.92 million, beating last month’s 4.9 million and analyst expectations of 4.9 million. The housing market was a bright spot for the U.S. economy in 2012 and is so far continuing its strength.

US Existing Home Sales data by YCharts.

The fifth and final economic release was the Conference Board’s Leading Economic Index, which was up 0.2% in January to 94.1, slightly below analysts’ expectations of 0.3% growth. The index is made up of 10 indicators and is designed to signal peaks and troughs in the business cycle. The index was led upward by growth in housing permits, signaling a strengthening economy.

On top of the negative reports, the market is also dealing with fallout from yesterday’s release of the minutes of January’s Federal Open Market Committee meeting. Certain Fed officials expressed disagreement with the Fed’s current $85 billion per-month purchases of assets. Markets have been buoyed by the Fed’s purchases, and now investors are worried that the gravy train will come to a halt.