The world’s largest home improvement retailer, The Home Depot, Inc. (NYSE:HD) has recently reported better-than-expected quarterly results on the back of a housing recovery. The company has started its fiscal year with a positive note and with a positive outlook; it is expecting further improvements in the future. This comes following disappointing results from its biggest rival Lowe’s Companies, Inc. (NYSE:LOW), the world’s second-largest home-improvement retailer, which missed both top- and bottom-line estimates.

![]()

Home Depot beats expectations

The Home Depot, Inc. (NYSE:HD)’s revenue rose 7.4% to $19.1 billion while its income increased by an impressive 18.5% to $1.2 billion, or $0.83 per share. The rebuilding efforts following Hurricane Sandy have caused a sales injection of $145 million. The results were significantly above the market’s expectations of $0.76 per share on revenue of $18.6 billion.

The better-than-expected results are largely due to the recovery in the housing market, which completely offset the negatives coming from unfavorable weather conditions and delays in tax refunds, which have hit almost every other retailer.

The Home Depot, Inc. (NYSE:HD)’s overall comparable-store sales increased by 4.3%, while the U.S. comparable-store sales increased by 4.8%. Customer transactions rose 2.5% and the average ticket price improved 5%.

In the previous quarter, the growth rate of The Home Depot, Inc. (NYSE:HD)’s professional-customer segment outperformed its consumer segment for the first time since 2008. This happened due to the resurgence of relatively smaller professional customers, i.e. those contractors who spend less than $10,000 a year. I believe that the increasing growth rate of this segment points toward improvements in the macroeconomic environment.

The Home Depot, Inc. (NYSE:HD) has now increased its annual earnings guidance from $3.37 a share to $3.52 a share and is also calling for a 2.8% increase in revenue as opposed to a 2% increase it announced earlier. But I don’t think that this is unusual as Home Depot has a habit of initially giving conservative guidance and then raising it later.

Interest rates

The record low interest rates are driving the housing boom, which translates into a healthy business environment for Home Depot and Lowe’s Companies, Inc. (NYSE:LOW). This was also evident in the quarterly results of Toll Brothers Inc (NYSE:TOL), the luxury home-builder, which has broken its seven-year order record.

Toll Brothers Inc (NYSE:TOL) announced its results on May 22. Its deliveries in terms of units increased by an impressive 33% and backlog climbed by 52% to 3,655 units. The company has beaten both top- and bottom-line estimates.

With demand increasing, prices are also going up and I expect this to continue in the coming quarters. The average price of signed contracts has increased by 15.9% to $678,000. Although its shares have struggled, the fundamentals of this niche player with few direct competitors are strong and I expect it to recover in the near term.

Lowe’s disappoints

On other hand, unlike Home Depot, Lowe’s sales were badly affected by cooler temperatures. Despite the “solid” performance of the indoor-merchandise unit, quarterly revenue still dropped by 0.5% to approximately $13.1 billion. Its net income rose by just 2.5% to $540 million or $0.49 per share, below analysts’ estimates of $0.51 per share on revenue of $13.4 billion.

Same-store sales also disappointed, posting a drop of 0.7% from the same quarter last year. This is in stark contrast to Home Depot’s results. I understand that Lowe’s is going through an overhaul; shutting down stores, changing the management structure, pushing toward “everyday low prices” and reviewing its product lines to better meet the customers’ needs. But the current results have shown that little improvements have been made so far and lots more needs to be done.

What makes Home Depot better?

Unlike Lowe’s, Home Depot’s management did an overhaul before the housing downturn, and as a result the company has been recording considerably better performance than its rival in the past few years. Most of its growth can be attributed to its transformational changes – including improving its supply chain and investing in its workforce — and now, as the housing sector starts picking up, Home Depot is at the front row capitalizing on the improving environment. On the other hand, as indicated earlier, Lowe’s is making the necessary changes now and I believe that it will take some time before its effects become apparent.

Eyeing the real estate recovery, Home Depot had already prepared a plan to target professional customers, which included increasing inventory of pro-focused products such as plywood and fast-drying paints, setting up of separate checkout counters and increasing sales efforts towards contractors. The result was that Home Depot ended up increasing its sales to professionals by 35% while Lowe’s could only manage 25%.

The higher professional sales also gave a boost to comparable-store sales and average ticket, two of the leading indicators in this industry’s earnings, which then drives the stock price. I believe that Home Depot’s strong pro-sales performance was one of the reasons behind its delivery of significantly better comparable-store sales than Lowe’s.

Conclusion

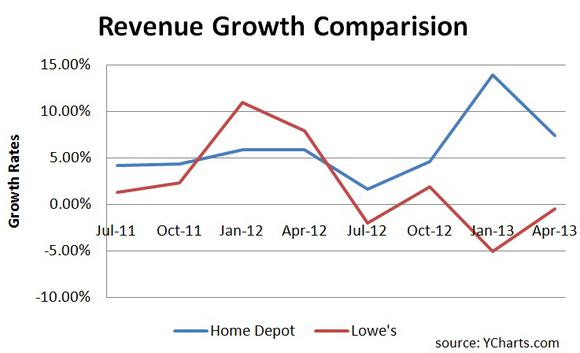

In short, effective marketing efforts and better merchandising have given Home Depot a significant lead over Lowe’s Companies, Inc. (NYSE:LOW). Home Depot’s investors should be pleased with the company’s proactive approach and I believe that this will give them more confidence in the top management. In the previous four quarters, Home Depot’s average growth was 6.91%, while Lowe’s, which has reported three year-over-year revenue drops in four previous quarters, has fallen by an average of 1.4%. This is shown in the picture below.

For the current quarter, investors should expect better performance from outdoor merchandise units of both Home Depot and Lowe’s Companies, Inc. (NYSE:LOW) due to the late start of the spring-garden season. Home Depot could post a significant increase in comparable-store sales, which could be even greater than its overall sales growth due to the seasonal shift.

Strong comparable-store sales numbers could drive the stock higher after the next earnings release. Investors should note that for the month of April, the comparable-store sales at Home Depot increased by as much as 10%.

For Lowe’s Companies, Inc. (NYSE:LOW), although the results were far from satisfactory, the company has reiterated its full-year guidance. Improvements are expected in the current quarter, particularly in May, as indicated by the chief executive Robert Niblock in the earnings call. However, due to the broader reasons explained above, I believe Home Depot’s second-quarter earnings will be better than Lowe’s.

Sarfaraz Khan has no position in any stocks mentioned. The Motley Fool recommends Home Depot and Lowe’s.

The article Home Depot Rises As Lowe’s Struggles originally appeared on Fool.com and is written by Sarfaraz Khan.

Sarfaraz is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.