The internet is a very competitive market. For less than $150 anyone can buy a small shared hosting package and start a website. With such low barriers it is easy to think that Google Inc (NASDAQ:GOOG) faces a great amount of competition. The reality is that the amount of financial capital and human capital required to make an operation which can compete with Google is enormous. It is easy to get lost in all of the talk of Google’s eminent demise. In reality Google is a secure player in multiple online sectors with huge barriers to entry.

According to one study, the major uses of the internet are e-mail, gathering information, online banking, sharing content, geographical navigation services, and online shopping. Google covers almost all of these services. Gmail, Google+, and Blogger help people communicate and share content. Google News is one of the most popular news sites in the world. Google Maps provides directions, and the recent fiasco with Apple’s map app shows just how difficult developing a good map app can be. Google Shopping helps people to shop online. Although it does not offer the same level of service as Amazon, it is still one of the top affiliate networks.

Google has built this empire while maintaining great financials. They have a total debt to equity ratio of .09 with $14.8 billion in cash and equivalents at the end of 2012. Their ROA of 11.8% and ROI of 14.9% are healthy. With a profit margin of 21.4% it is easy for the company to maintain steady free cash flow to invest in their operations and fund acquisitions.

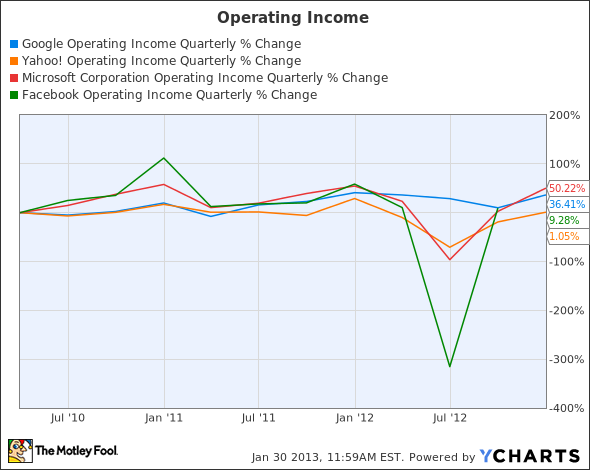

GOOG Operating Income Quarterly data by YCharts

How Does the Competition Compare?

The above chart shows how Yahoo! Inc. (NASDAQ:YHOO)‘s operating income has not grown at the same rate as Google’s or Microsoft Corporation (NASDAQ:MSFT)’s. Yahoo!’s CEO, Marissa Mayer, has not been with the company for a long time but she still has her work cut out for her. Yahoo! does not have the strong search business to fall back on like Google. Yahoo! Mail and Yahoo! News are both popular products, but they do not offer the same competitive advantage as a profitable search business. For the first three quarters of 2012 display page views decreased 5%, while search page views decreased 13% relative to the same period in 2011. Nevertheless, Yahoo!’s ROA of 19.4% and ROI of 25.3% are encouraging. Even with a clean balance sheet with no debt, the lack of operating income growth over the past couple years is concerning. For years Yahoo! and Google have fought back and forth, and yet Google has been able to grow a larger product suite and provide more operating income growth.

Google strikes fear into the heart of Microsoft Corporation (NASDAQ:MSFT), and with good reason. On the consumer front Microsoft is facing a number of headwinds. Google’s Android has much greater market share than Microsoft’s smart phone offerings. Also, the adoption rate of Windows 8 appears to be rather depressed. The state of Microsoft in the online search market is not that encouraging. In the last two quarters of 2012 Microsoft’s online services division posted an operating loss of $647 million. This is less than the $973 million operating loss posted in the last two quarters of 2011, but after years of experience in this market it is disconcerting that Microsoft is still unable to turn a profit. The company’s balance sheet is clean with a total debt to equity ratio of .17. Their ROI of 20.0% and ROA of 12.9% are strong, along with their profit margin of 21.7%. Nevertheless, the technology and consumption patterns are changing, and Microsoft’s future prospects are unclear.

Facebook Inc (NASDAQ:FB) is the newest player to come to the party. The company effectively meets people’s need to communicate and share content, but is lacking in other areas. Mark Zuckerberg recently announced the new graph search, which is stirring up major privacy concerns. This new search product is not a wide reaching search engine, but instead is focused on using user’s data in a new way. The news feed offers news and updates but Facebook does not have a serious news product like Google News or Yahoo! News. Like the other firms Facebook has almost no debt, with a total debt to equity ratio of .06. The large growth prospects are constantly touted, but right now the company has an ROA of 1.8% and an ROI of 2.0%. Their profit margin of 6.3% is low compared to the competition. Facebook promises growth and earnings, but Microsoft has tried this for years and is still waiting to turn a profit in their online services division. Facebook’s social network gives the company a unique and powerful asset. Regardless, Google still has a major advantage over Facebook with their dominant position in the search market.

Conclusion

Fundamentally, Google is a strong company. The firm employs thousands of top notch engineers. Coupled with their custom data centers, they own billions of dollars in assets, which make it prohibitively expensive for any potential competitor to try and compete. They have grown their dominant position in search to offer a host of supplementary services which cover almost all of the major reasons for which people use the internet. Android continues to make gains in mobile. Google is a growing company with a wide moat, and as such is a great long term investment.

The article Should Google be Afraid of the Competition? originally appeared on Fool.com and is written by Joshua Bondy,

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.