Every investor has a story about the big winner they missed. Consider Starbucks Corporation (NASDAQ:SBUX), which grew from a single Seattle cafe into a worldwide retail titan. Since the company’s initial public offering in June 1992, Starbucks has earned 9,340% for investors.

Today, Starbucks is a mature business. So for big profits, investors should be looking for the next Starbucks among smaller companies with similar characteristics, a long growth runway, and a reasonable valuation.

So, does Panera Bread Co (NASDAQ:PNRA) meet that criteria? Here’s three reasons why Panera could be the next multi-bagger.

Rapid growth

Panera is in a marketplace sweet spot. Consumers are looking to substitute burgers and fries for wholesome food at reasonable prices.

And this is exactly what Panera Bread Co (NASDAQ:PNRA) offers. High quality meals with an emphasis on fresh ingredients and antibiotic-free meats.

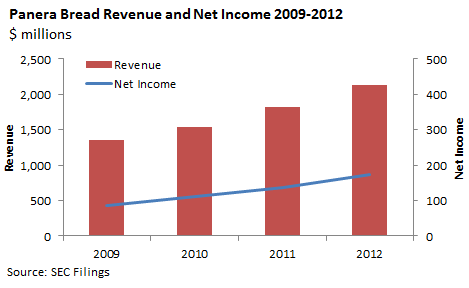

Results are showing up on the financial statements. Over the past five years, sales and earnings have grown at a 15% and 25% annual clip, respectively.

Going forward, analysts project Panera to grow its EPS at a 20% rate over the next five years driven by three factors:

Expansion: The company has the potential to double its store count in the United States with international markets almost completely untapped.

Same Store Sales: Panera Bread Co (NASDAQ:PNRA) is growing same-store sales at a mid-single digit clip. The company’s catering service is gaining momentum and now accounts for 8% of total revenue. Panera is also driving traffic through new menu items like the shrimp and soba noodle salad. Yum!

Margins: Falling wheat prices and labor costs should allow Panera to expand margins.

Perhaps, the biggest threat to Panera may be Starbucks Corporation (NASDAQ:SBUX) itself. Last summer, the company acquired La Boulange for $100 million in an effort to beef up its food offerings.

Today, only one third of Starbucks’ transactions involve a food item. But management is betting better sandwiches and biscuits could increase traffic and steal sales from rivals like Panera.

Execution

Founder Ron Shaich is one of the most successful CEO’s in history. Shaich has over 30 years of experience in the retail business and has built 1,600 stores across North America. Under his leadership, Panera has become the 14th largest fast-food chain in the United States.

Panera’s financials are in even better shape. The company has no long-term debt, which gives management ample financial flexibility to execute its growth strategy.

In addition, last year, the company generated $290 million in cash flow from operations which is more than enough to fund the company’s expansion.

Reasonable valuation

This bothers me. Nearly every article I’ve read on Panera Bread Co (NASDAQ:PNRA) goes like this: Great company…great growth…but looks a little too expensive. After a 260% run over the past five years, Wall Street has declared you missed the move. But, let’s take a look at the metrics. Panera trades at 23 times forward earnings. Given EPS is expected to grow at a 20% clip over the next five years, the stock is valued at a reasonable 1.15 PEG ratio. That’s pretty cheap compared to other names in the space.

Consider Chipotle Mexican Grill, Inc. (NYSE:CMG). This stock trades at a monster 30 times forward earnings. Assuming a 20% growth rate, Chipotle is valued at a premium 1.50 PEG ratio.Such a premium is troubling given the company’s deteriorating fundamentals.

Last quarter, the company grinded out a meager 1% gain in comparable store sales. Chipotle’s margins are also under pressure due to higher prices for barbacoa, steak, and salsa ingredients.

Panera looks even cheaper against restaurant king McDonald’s Corporation (NYSE:MCD)?

McDonald’s looks pretty cheap at 15 times forward earnings, but that’s misleading given the company’s slowing 9% EPS growth rate.

After a great run, the company is running into the law of large numbers with same store sales declining 1% in the first quarter.

But why such a premium? Interest starved investors are in a desperate hunt for yields. This could leave the stock particularly vulnerable if interest rates start rising.

Foolish bottom line

In many ways, Panera Bread Co (NASDAQ:PNRA) exhibits the same traits Starbucks Corporation (NASDAQ:SBUX) did 10 years ago. Big growth, great execution, and a reasonable valuation is a winning combination that could propel shares higher.

Robert Baillieul has no position in any stocks mentioned. The Motley Fool recommends Chipotle Mexican Grill, McDonald’s, Panera Bread, and Starbucks. The Motley Fool owns shares of Chipotle Mexican Grill, McDonald’s, Panera Bread, and Starbucks.

The article Is This Stock the Next Starbucks? originally appeared on Fool.com.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.