![]()

More margin pressure

In common with Dollar General Corp. (NYSE:DG), Family Dollar Stores, Inc. (NYSE:FDO) is seeing margin pressure as its sales mix shifts towards lower-margin consumables and away from higher-margin discretionary items. In fact, the share of consumables rose to 72.5% of total sales, compared to 68.9% last year. In contrast, Dollar Tree, Inc. (NASDAQ:DLTR) managed to benefit from margin expansion by growing its sales mix in the other direction. However, this appears to be an isolated case amongst the mass market retailers.

Family Dollar actually highlighted industry data that suggested that its typical consumer was spending less in the marketplace, but more at its stores. This is not a great sign for the economy. This data also implies that if there is growth to be generated, it will come at the expense of its competition. Family Dollar Stores, Inc. (NYSE:FDO) is likely taking share from the supermarkets within the grocery category. Unfortunately, consumables like tobacco and groceries are not really high-margin items. So even as Family Dollar expands sales in these areas, it will not see gross margin expansion.

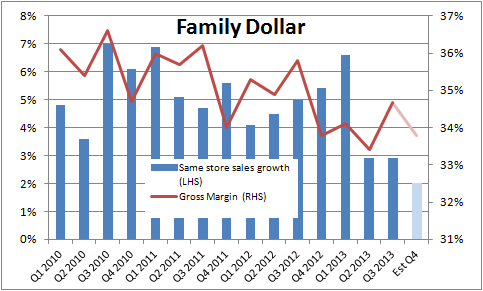

These trends are nicely illustrated with a look at the company’s sales and margin trends over the last few years. Note the company’s forecast for the next quarter is for an anemic-looking 2% same store sales growth. This is a bit disappointing, because even though the first quarter was weak for most retailers due to a number of issues (payroll tax increases, tough weather comps, tax refund delays and the sequester), the second quarter was supposed to be a more favorable environment.

On the other hand, the positive news is that gross margins were forecast to be almost flat in the next quarter, much to the liking of the markets.

Why the market likes these results

The real takeaway of these results is how Family Dollar Stores, Inc. (NYSE:FDO) is adjusting to a slower sales environment. Gross margins were predicted to be almost flat in the fourth quarter, and in the conference call, the management discussed the possibility for them to be flat in 2014 as well. There are a number of reasons for a more positive outlook for both gross and operating margins:

- The company has adjusted to the slower sales environment and is now highly focused on reducing things like freight, distribution center, and advertising costs.

- It is starting to lap the unfavorable mix shift movements from last year, so comparisons will get easier.

- Management spoke of some recent improvements in its core discretionary businesses and spoke of the beginnings of stabilization.