ManpowerGroup’s analysis versus peers uses the following peer-set: Adecco S.A. (ADEN), Randstad Holding nv (AMS:RAND), Robert Half International Inc. (NYSE:RHI), Michael Page International plc (LON:MPI), Hays plc (LON:HAS), Korn/Ferry International (NYSE:KFY) and Kelly Services, Inc. (NASDAQ:KELYA). The table below shows the preliminary results along with the recent trend for revenues, net income and returns.

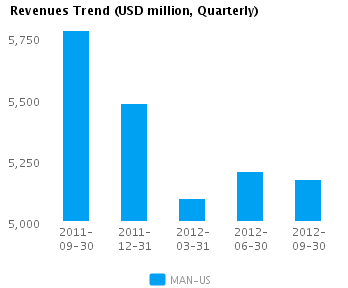

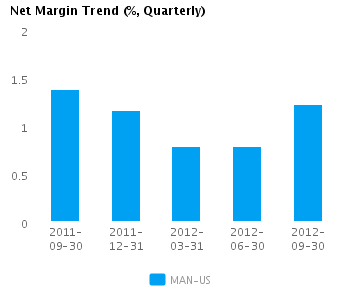

| Quarterly (USD million) | 2012-09-30 | 2012-06-30 | 2012-03-31 | 2011-12-31 | 2011-09-30 |

|---|---|---|---|---|---|

| Revenues | 5,172.3 | 5,206.7 | 5,096.4 | 5,484.0 | 5,782.3 |

| Revenue Growth % | (0.7) | 2.2 | (7.1) | (5.2) | 2.0 |

| Net Income | 63.1 | 41.0 | 40.2 | 63.6 | 79.6 |

| Net Income Growth % | 53.9 | 2.0 | (36.8) | (20.1) | 9.5 |

| Net Margin % | 1.2 | 0.8 | 0.8 | 1.2 | 1.4 |

| ROE % (Annualized) | 9.9 | 6.5 | 6.4 | 10.2 | 12.5 |

| ROA % (Annualized) | 3.6 | 2.4 | 2.3 | 3.6 | 4.4 |

Valuation Drivers

ManpowerGroup trades at a lower Price/Book multiple (1.2) than its peer median (2.9). The market expects MAN-US to grow earnings about as fast as the median of its chosen peers (PE of 14.4 compared to peer median of 15.2) but not to expect much improvement in its below peer median rates of return (ROE of 8.2% compared to the peer median ROE of 11.8%).

The company’s profit margins are below peer median (currently 1.0% vs. peer median of 2.2%) while its asset efficiency is about median (asset turns of 3.0x compared to peer median of 2.9x). MAN-US’s net margin is similar to its five-year average net margin of 0.6%.

Economic Moat

The company enjoys both better than peer median annual revenue growth of 16.6% and better than peer median earnings growth performance 195.4%. MAN-US currently converts every 1% of change in annual revenue into 11.7% of change in annual reported earnings. We view this company as a leader among its peers.

MAN-US’s return on assets is less than its peer median currently (3.0% vs. peer median 5.4%). It has also had less than peer median returns on assets over the past five years (1.9% vs. peer median 4.8%). This performance suggests that the company has persistent operating challenges relative to peers.

The company’s gross margin of 17.2% is around peer median suggesting that MAN-US’s operations do not benefit from any differentiating pricing advantage. In addition, MAN-US’s pre-tax margin is less than the peer median (1.9% compared to 3.3%) suggesting relatively high operating costs.

Growth & Investment Strategy

While MAN-US’s revenues growth has been below the peer median in the last few years (0.7% vs. 1.1% respectively for the past three years), the market still gives the stock an about peer median PE ratio of 14.4. The market seems to see the company as a long-term strategic bet.

MAN-US’s annualized rate of change in capital of -2.5% over the past three years is less than its peer median of -1.1%. This below median investment level has also generated a less than peer median return on capital of -0.2% averaged over the same three years. This outcome suggests that the company has invested capital relatively poorly and now may be in maintenance mode.

Earnings Quality

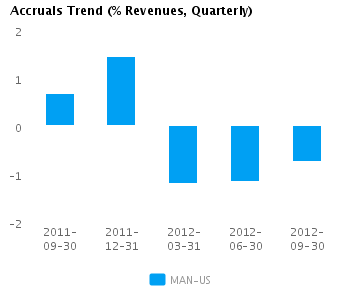

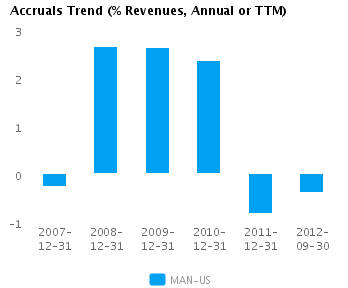

MAN-US reported relatively weak net income margins for the last twelve months (1.0% vs. peer median of 2.2%). In addition, the company has booked a relatively low level of accruals (-0.4% vs. peer median of 0.2%) for the same period. Combined, these factors suggest that the reported net income numbers might have likely benefitted from some amount of underaccruals.

MAN-US’s accruals over the last twelve months are around zero. However, this modestly negative level is also less than the peer median which suggests some amount of draining of reserves.

Trend Charts