report and conference call as well as take a look at the future prospects domestically and internationally for the company.

Fourth quarter highlights:

1). 3.2% Dunkin’ Donuts U.S. comparable store sales growth

2). Added 256 net new restaurants worldwide including 149 net new Dunkin’ Donuts in the U.S.

3). Adjusted operating income up 16.1% on a 13-week basis

4). Adjusted operating income margin to 47.6%

5). Adjusted EPS up approximately 21% to $0.34 on a 13-week basis

6). Board of Directors declare $0.19 first quarter dividend for a 27% increase over the company’s fourth quarter 2012 dividend

In the report, Nigel Travis, Chief Executive Officer and President of Dunkin’ Donuts U.S., had this to say about the quarter:

“We have the unique combination of strong brand heritage and significant U.S. and global restaurant expansion opportunities, which we are capitalizing on to drive profitable growth for both our franchisees and shareholders. Our contiguous, strategic development approach is working, and we’re excited to begin selling Dunkin’ Donuts franchises in California. Despite macro-economic instability and a tough competitive environment, consumer and franchisee demand for Dunkin’ Donuts is high, our franchisee relationships are strong, and we continue to leverage our asset-light business model giving us confidence to target 15 percent plus adjusted earnings per share growth in 2013.”

Domestic story

The company reported it now has 7,306 points of distribution, which is 291 points higher than last year. The company recently announcedits plans for westward expansion into the previously untapped markets of Southern California by 2015. I currently live in California myself but attend school on the east coast. Since making the transition to the east coast, I have become a daily Dunkin’ Donuts patron myself due to the fast service and the many locations that surround my campus. I am very confident that the brand will thrive in California as the company has built a strong U.S. brand and offers high quality options for a reasonable price.

In addition, the western climate will benefit the cold coffee items which dominate the current menu. The company wants to add 330 to 360 new stores this year in both its new markets and existing markets. The long term goal is to grow the distribution points by 5% yearly up to a total of 15,000 locations. I will be looking to see if the company can expand its distribution points while meeting analyst expectations of strong same store sales growth. The company seems to be controlling its expansion to reasonable rates as I am sure they have learned from

Starbucks Corporation (NASDAQ:SBUX)’s past overexpansion problems. Previously, Starbucks saturated the market by expanding its store base far too quickly. However, I still remain concerned that growth could be slowed by Starbucks’s plans to increase its U.S. store count by 1,500 locations. I believe the U.S coffee market will absorb the additional stores as I have confidence that Howard Schultz, president and chief exective officer, won’t allow the company to overexpand again. Lastly, Starbucks will be adding drive through options to many of its new and old stores which will compete directly with Dunkin’ Donuts.

International story

The company was very positive when it came to its international growth potential. The company reported its Dunkin’ Donuts international distribution points grew by 105 points to a total of 3,173 locations. Dunkin’ Donuts international increased its revenues 2.9% from the prior year. In the future the company will look to expand further into India, Vietnam, Russia, China, and Brazil to fuel its international growth rates. In 2013, the goal is to open 400 to 500 new locations between both brands. Over the next 10 years the company plans to open roughly 250 new Baskin-Robins locations while also expanding its Dunkin’ Donuts brand. In China and India, coffee demand is rising and the company should accelerate its growth plans to try and keep pace with Starbucks. Both these countries are becoming huge coffee markets and if Dunkin’ misses the boat I am afraid they will be presented with a much tougher landscape in the future.

Product innovation

On the conference call the company was very pleased with the progress made in expanding its current menu offerings. The company has been shifting its menu to allow regular customers to upgrade from just a donut to Breakfast Burritos, Red Velvet Donuts, and an array of sandwiches. The pipeline for future menu options is as long as it has ever been and new products are being welcomed with open arms. The expansion of the product line has shown to be key for increasing comparable same store sales as 75% of the growth came from higher tickets. In addition, these new products carry high margins which will greatly increases profitability for the franchisees as consumers add on to their coffee orders. By expanding the menu, the company can better differentiate itself from the many coffee alternatives on the market.

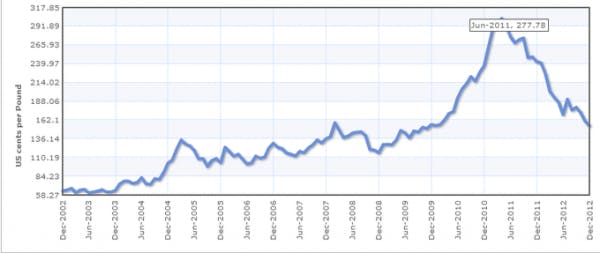

Falling commodity costs

Currently, coffee prices have fallen to their lowest level since the middle of 2010 and have decreased significantly since the multi-year highs set in 2011. Dunkin’ and many competitors use Arabica beans for their coffee products. Below is a chart of the price of Arabica beans over the last 10 years:

Source: IndexMundi

The company expects its franchisees will experience lower commodity costs in 2013 as a result of the very low coffee prices. The lower coffee prices will help franchisees adjust to the rising costs for wheat caused by the drought. The longer the price of inputs stays low, the longer the franchisees will be able to generate especially high profit margins, which will benefit the entire company.

Conclusion

The company is well positioned to grow its brands domestically and internationally. I believe the company should work on speeding up the expansion into China and India as a failure to set strong footing in these regions would be very detrimental in the long run. I am very pleased to see ticket sales being driven higher by the popular new additions to the menu. As patrons increasingly trade up to the new products profit margins will rise for franchisees. As coffee prices continue to decline, the franchisees will continue to see their cost of goods sold decrease. I remain very bullish on the entire coffee space as global coffee demand continues to rise. Also, let’s not forget the company is now paying investors an attractive 2% dividend yield.

The article Dunkin’ Brands Group (NASDAQ:DNKN) Earnings Analysis originally appeared on Fool.com and is written by Nathaniel Matherson.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.