In the January/February issue of the Harvard Business Review, three scholars from INSEAD in France compiled a ranking of the 100 best CEOs in the world who took office between 1995 and 2010. While Steve Jobs of Apple Inc. (NASDAQ:AAPL) unsurprisingly garnered the top spot, Amazon.com, Inc. (NASDAQ:AMZN) founder and CEO Jeff Bezos was ranked No. 2. Due to Jobs’ untimely passing in 2011, that makes Bezos the greatest CEO alive, according to the HBR study.

The ranking system

The authors’ goal was to create an objective measure of long-term CEO performance. To judge CEO performance, the authors measured total shareholder returns and increase in market capitalization over each CEO’s tenure. The authors rejected subjective measures of performance, as well as measures that were not comparable across industry groups: “Other metrics, such as sales, profitability, and innovation rates, are useful, too, but they differ by industry, which makes comparisons difficult.”

Amazon’s current market capitalization of approximately $120 billion makes a compelling case for putting Bezos at the top of the list of best CEOs. However, in an interview with HBR editor Adi Ignatius, Bezos himself cites legendary investor Ben Graham’s statement: “In the short term, the stock market is a voting machine. In the long term, it’s a weighing machine.” If we look back just a little more than four years, Amazon’s market capitalization was less than $25 billion.

Amazon Market Cap, data by YCharts.

If the study had been performed four years earlier, Bezos would not have fared nearly as well. This merely highlights that stock performance itself is an inherently subjective measure in the short term. To better evaluate Bezos’ performance, it is critical to look at trends in cash flow and profitability, as well as revenue, because Amazon’s stock price will be unsustainable without growth in these key metrics.

Amazon’s growth trend

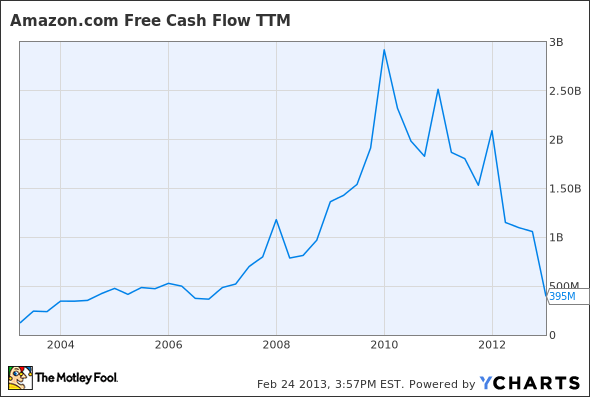

In the HBR interview, Bezos states that Amazon does not try to optimize its profit margin, but instead seeks to maximize long-term free cash flow. Amazon saw consistent growth in this metric for most of the last decade, but free cash flow has dropped precipitously over the past few years after peaking just below $3 billion in 2009.

Amazon TTM Free Cash Flow, data by YCharts.

The culprit has been a sharp increase in capital investment. Operating cash flow has risen each year since 2009, albeit slowly, growing from $3.29 billion to $4.18 billion over that time (a CAGR of 8.3%). However, capex has skyrocketed from $373 million in 2009 to $979 million in 2010, $1.81 billion in 2011, and $3.79 billion in 2012.

The investment community appears to be confident that these heavy capital expenditures have paved the way for rapid growth going forward. Thus far, there is not much evidence to support that contention. Amazon’s sluggish growth in operating cash flow can perhaps be blamed upon the rapid addition of distribution centers, which generate operating expenses upon opening, but may not be fully utilized for years. However, Amazon’s slowing revenue growth is more troubling.

Amazon Revenue Growth, data by YCharts.

While revenue grew 39.6% in 2010 and 40.5% in 2011, growth dropped off to 27% in 2012 despite the increasing pace of investment. Revenue growth hit a multiyear low of 22% in the fourth quarter, and Amazon projected a similar level of growth for the current quarter.

Competitors fighting back

Slowing growth at Amazon can probably be attributed to competitors finally fighting back. Several retailers experimented with price-match strategies during the holiday season, and Target Corporation (NYSE:TGT) announced last month that it would match prices from Amazon and other top online retailers year-round. Best Buy Co., Inc. (NYSE:BBY) followed suit with a year-round price-matching policy earlier this month. While discount leader Wal-Mart Stores, Inc. (NYSE:WMT) has avoided price-matching, the company’s current long-term strategy involves reducing operating expenses by 100 basis points and then “investing in price”: i.e., lowering prices to attract more customers.

Discount retailers like Wal-Mart, Target, and Best Buy are thus stepping up price competition with Amazon. As I discussed in a previous article, these three companies are equivalent in scale to Amazon (and Wal-Mart is nearly eight times larger) and have competitive operating expenses. Amazon thus has little or no inherent competitive advantage versus Wal-Mart, Target, or Best Buy. With these discounters having now implemented better strategies for competing against Amazon, the latter will have a tougher time gaining market share in the future.

Conclusion: The jury’s out

There are good reasons to doubt that Amazon will produce as much profit as investors seem to expect. Competitors are fighting back, and Amazon’s heavy investments over the past three years have not borne fruit in the form of better sales or earnings trends yet. It is possible that Amazon will eventually hit a tipping point, leading to a rapid rebound in profitability and accelerating revenue growth. However, until that happens, it is too early to crown Jeff Bezos the greatest CEO alive.

The article Is Jeff Bezos the Greatest CEO Alive? originally appeared on Fool.com and is written by Adam Levine-Weinberg.

Fool contributor Adam Levine-Weinberg owns shares of Apple. Adam Levine-Weinberg is short shares of Amazon.com. The Motley Fool recommends Amazon.com and Apple. The Motley Fool owns shares of Amazon.com and Apple.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.