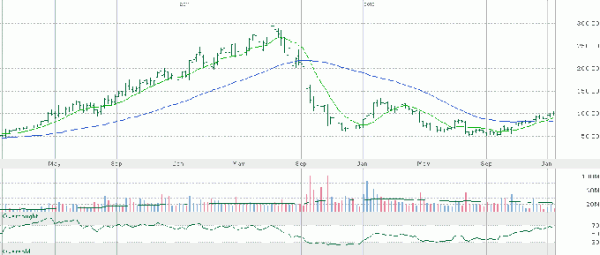

Netflix has had a rough time over the last year and a half. The stock reached a high of over $300 in mid-2011; a few bad quarters and analyst downgrades later, and the Netflix, Inc. (NASDAQ:NFLX) faithful watched in horror as their shares plummeted, finally reaching a low of $52.81 in July of 2012. Since then, the stock has bounced nicely off its lows, settling at $101.69 as of this writing. Going into their earnings report next Wednesday, I have to ask: What happened to the concerns that caused Netflix to almost double during the second half of 2012? And what about the strong competition that was ignored for so long during Netflix’s stellar climb? Unless the company can adequately answer these questions, I’m not sure that the recent rally was justified.

Netflix’s strategy is to grow its subscriber base throughout the world by continually improving the delivery of their products, with a particular focus on their streaming video offerings. The trend has been toward Internet-based content and away from DVD’s, and the company expects the DVD side of its business to drastically shrink in the future. So, Netflix wants to provide the best possible customer experience using the latest technologies while maintaining an adequate profit margin.

In addition, there are more Internet-based providers than ever before, such as Amazon.com, Inc. (NASDAQ:AMZN)’s Prime Video, Hulu.com, and YouTube. For those customers who prefer DVD’s to streaming video, kiosks by Blockbuster and Redbox are popping up all over the country. It seems that renting a movie while grocery shopping is more convenient to some than waiting for a DVD in the mail. The aspect of the earnings call that I will be paying the most attention to is any discussion by Netflix of its competition and how they intend to deal with the various types of competitors mentioned here.

Even with a terrible year earnings-wise in 2012 and all of the competition, Netflix still trades at an extremely high valuation, even when compared to projected future earnings. Consensus estimates call for earnings of just 4 cents per share this year, so a P/E ratio isn’t very meaningful. In 2013 and 2014, analysts are calling for earnings of $0.40 and $1.40 respectively, and even if Netflix achieves this, that means it is trading at 73 times 2014’s earnings.

I’m not particularly concerned with the earnings numbers themselves at this point in the game. I want to know how, despite all of the factors working against them, Netflix is planning to grow its profitability to a point that justifies the astronomic valuation of the stock.

The article Netflix Earnings Preview: Why so Expensive? originally appeared on Fool.com.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.