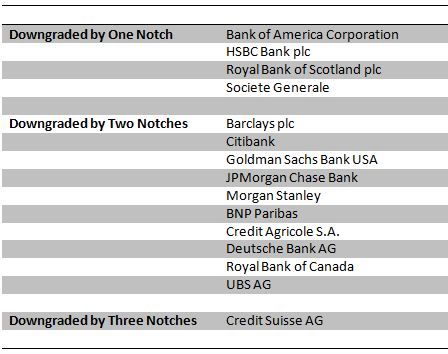

What other Credit Rating Agencies have been doing one step at a time, Moody’s did that and much more in a single stroke. After markets all over the globe had closed Moody’s went ahead and downgraded 15 major banks across Europe, America and Canada.

4 banks got downgraded by a notch, 10 got downgraded by 2 and one lost 3 notches.

In the press release accompanying the downgrade here is what Moody’s says:

RATINGS RATIONALE — STANDALONE CREDIT DRIVERS

–FIRST GROUP

The first group of firms includes HSBC, Royal Bank of Canada and JPMorgan. Capital markets operations (and the associated risks) are significant for these firms. However, these institutions have stronger buffers, or ‘shock absorbers,’ than many of their peers in the form of earnings from other, generally more stable businesses. This, combined with their risk management through the financial crisis, has resulted in lower earnings volatility. Capital and structural liquidity are sound for this group, and their direct exposure to stressed European sovereigns and financial institutions is contained.

Firms in this group now have standalone credit assessments of a3 or better (on a scale from aaa, highest, to c, lowest). Their main operating companies now have deposit ratings of Aa3, and their holding companies, where they exist, have senior debt ratings between Aa3 and A2. Their short-term ratings are Prime-1 at both the operating and holding company level.

–SECOND GROUP

The second group of firms includes Barclays, BNP Paribas, Credit Agricole SA (CASA), Credit Suisse, Deutsche Bank, Goldman Sachs, Societe Generale and UBS. Many of these firms rely on capital markets revenues to meet shareholder expectations. Their relative position reflects a combination of differentiating and sometimes adverse factors. Capital markets operations constitute a large part of the overall franchises for Credit Suisse, Goldman Sachs, Barclays, and Deutsche Bank, but less so for UBS, Societe Generale, BNP Paribas and CASA’s cooperative group, Groupe Credit Agricole.

Other factors contribute to the relative positioning. For example, Barclays, BNP Paribas and Groupe Credit Agricole have, to varying degrees, relatively robust shock absorbers. Exposure to capital markets businesses is very high for Goldman Sachs, but this is balanced by a record of effective risk management. Barclays, BNP Paribas, Groupe Credit Agricole, and Deutsche Bank also have sizeable but varying degrees of exposure to weaker European economies. Some firms are relatively weak with regard to structural liquidity or reliance on wholesale funding.

Firms in this group now have standalone credit assessments of baa1 or baa2. Their deposit ratings range between A1 and A2, and their short-term ratings are Prime-1 at the operating company level. Their holding companies, where they exist, have senior debt ratings between A2 and A3 and short-term ratings between Prime-1 and Prime-2.

–THIRD GROUP

The third group of firms includes Bank of America, Citigroup, Morgan Stanley, and Royal Bank of Scotland. The capital markets franchises of many of these firms have been affected by problems in risk management or have a history of high volatility, while their shock absorbers are in some cases thinner or less reliable than those of higher-rated peers. Most of the firms in this group have undertaken considerable changes to their risk management or business models, as required to limit the risks from their capital markets activities. Some are implementing business strategy changes intended to increase earnings from more stable activities. These transformations are ongoing and their success has yet to be tested. In addition, these firms may face remaining risks from run-off legacy or acquired portfolios, or from noteworthy exposure to the euro area debt crisis.

Firms in this group now have standalone credit assessments of baa3. Their deposit ratings are A3 at the operating company level. Their holding companies, where they exist, have senior debt ratings between Baa1 and Baa2. Their short-term ratings are Prime-2 at both the operating and holding company level.

Given that this move was much anticipated by the market, it remains to be seen how markets choose to react to it.